Adoption Is Mechanical

BNPL, Stablecoins, and How Financial Infrastructure Actually Changes

In 2019, large merchants integrating Buy Now, Pay Later reported conversion lifts of 30% to 50% and average order value increases of up to 87% within weeks of deployment. No regulatory clarity existed at the time. No consumer advocacy consensus had formed. No payments standards body had issued guidance. Adoption occurred anyway because the mechanism was immediate and measurable. Cart abandonment fell. Revenue rose. Competitive pressure followed.

That sequence matters. BNPL did not enter the financial system through persuasion or narrative acceptance. It entered because a specific friction was quantified and resolved inside an existing workflow. Cryptocurrency and blockchain infrastructure are now entering institutions through an analogous mechanism. However, the analogy is structural, not scalar, and not temporal. The friction is different. The workflow is different. The depth of integration is… different. The adoption logic is the same.

BNPL offers a nice reference case. It’s a demonstration of how financial service adoption can proceed when friction is visible at the surface and feedback loops operate quickly. Crypto infrastructure demonstrates something a bit different. How adoption must proceed when friction is structural and institutional, embedded at layers that inherently resist rapid iteration. This asymmetry governs nearly everything that follows.

The comparison to BNPL is not about equivalence in scale, volatility, or audience. BNPL operated at the checkout layer with consumer pull and merchant incentives. Stablecoins and tokenized settlement infrastructure operate at treasury, custody, and compliance layers under institutional gating. The analogy is about sequencing. In both cases, adoption followed measurable operational improvement once regulatory conditions permitted deployment. The layers differ. The mechanics rhyme. This essay examines how financial infrastructure becomes economically rational, and why crypto’s path is slower, less visible, and structurally constrained.

Surface Plug-in. Structural Integration.

The most important distinction between BNPL and crypto adoption is not use case or scale. It is embedding depth.

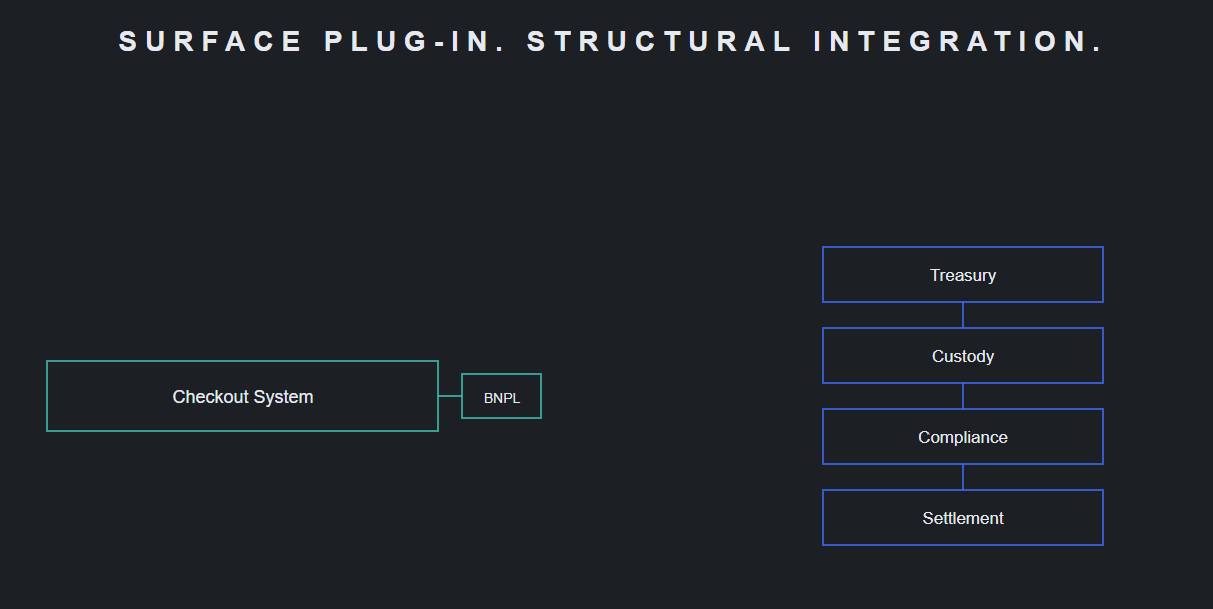

BNPL succeeded because it integrated into existing payment workflows without requiring structural change. Merchants did not replace credit cards. They added an option at checkout. Integration often occurred within 24 hours through standardized APIs. Consumers continued using cards alongside BNPL. The system layered on top of existing rails.

This shallow embedding produced fast feedback loops. Conversion increased. Merchants reinvested. Competitors followed. Consumer expectations shifted. BNPL became a default choice rather than a differentiated feature. By 2024, PayPal alone processed more than $33 billion in global BNPL volume, a 21% increase over the prior year. The mechanism scaled precisely because it required no fundamental workflow redesign.

Crypto infrastructure gets embedded differently. Stablecoins, tokenized deposits, and on-chain settlement integrate at the treasury, custody, and reconciliation layers. These systems do not surface at checkout. They operate behind enterprise interfaces. By design, end users do not know which rail was used. The embedding is structural rather than cosmetic.

This depth creates a first-order constraint on adoption dynamics. Integration touches core financial plumbing: how collateral moves, how counterparty exposure is calculated, how liquidity is allocated across time zones. Changes require integration into risk systems, accounting treatment, and compliance reporting. When Visa launched USDC settlement in the United States in late 2025, the value proposition was explicit: seven-day settlement windows instead of five, automated treasury operations, and operational resilience across weekends and holidays. Banks like Cross River and Lead Bank began settling with Visa in USDC over the Solana blockchain. This wasn’t an experiment, but live infrastructure. The timeline from pilot to production, however, spanned years.

The implication is not that crypto adoption is weaker. It is that feedback loops are slower, visibility is lower, and iteration cycles are longer. BNPL could demonstrate value in weeks. Crypto infrastructure demonstrates value in quarters or years. The depth of embedding determines the speed of feedback, while masking the strength of demand.

Adoption Begins When Friction Becomes Measurable

BNPL adoption accelerated when merchants stopped debating whether installment payments were good for consumers and started observing what happened to checkout metrics. A common misconception is that the primary friction was about credit access. It was payment size and timing. Consumers abandoned carts at rates approaching 70% when forced into full upfront payment. That friction was already visible in merchant analytics. BNPL translated it into revenue recovery.

No consumer demanded BNPL in surveys. Demand expressed itself indirectly through behavior. Merchants measured abandonment. They measured basket size. They measured repeat purchase rates. When BNPL providers absorbed credit risk and returned higher conversion, the decision to embed became operational more than strategic.

Crypto infrastructure adoption follows the same logic, but the friction is institutional rather than consumer-facing. Settlement delays of two to three business days in correspondent banking systems trap substantial capital in prefunded liquidity positions. Estimates of capital held in nostro and vostro accounts globally vary widely (industry reports cite figures ranging from $5 trillion to $28 trillion) but the directional point is more important than the precise magnitude. Capital is parked across currencies and time zones as defensive liquidity, unavailable for productive deployment. Cross-border wires cost between $25 and $50 per transaction through SWIFT-based channels, with settlement windows stretching one to five business days depending on corridor, cut-off times, and currency conversion requirements.

The scale of trapped capital creates measurable drag. Treasury teams quantify this through working capital audits and reconciliation timelines. The friction is expressed in hours, basis points, and balance sheet inefficiency rather than checkout abandonment. The G20 Roadmap for Enhancing Cross-Border Payments has set explicit targets: reduce average retail payment costs below 1% and remittance costs below 3% by 2030. While some see these as aspirational statements, they are really an acknowledgment that current friction levels are economically significant enough to warrant multilateral coordination.

Stablecoins and tokenized settlement can resolve portions of this friction mechanically. Transactions settle in minutes rather than days. Capital is released from prefunded accounts. Reconciliation becomes atomic. Transferring USDC via Solana, for example, costs less than $0.01 in network fees and settles in under five seconds. The comparison to traditional correspondent channels ($25–$50, one to three days) is stark on a per-transaction basis.

This does not mean correspondent banking will disappear or that crypto rails will replace traditional settlement infrastructure at scale. What it means is that where speed, cost, and availability matter at the margin (specific corridors, use cases, and counterparty relationships) crypto infrastructure offers a measurable alternative. Institutions do not need to believe in crypto to observe these effects. They need only measure settlement duration and liquidity utilization in contexts where the comparison is relevant.

In both cases, adoption began when friction crossed from tolerated inefficiency into measurable loss.

Late Correction. Early Permission.

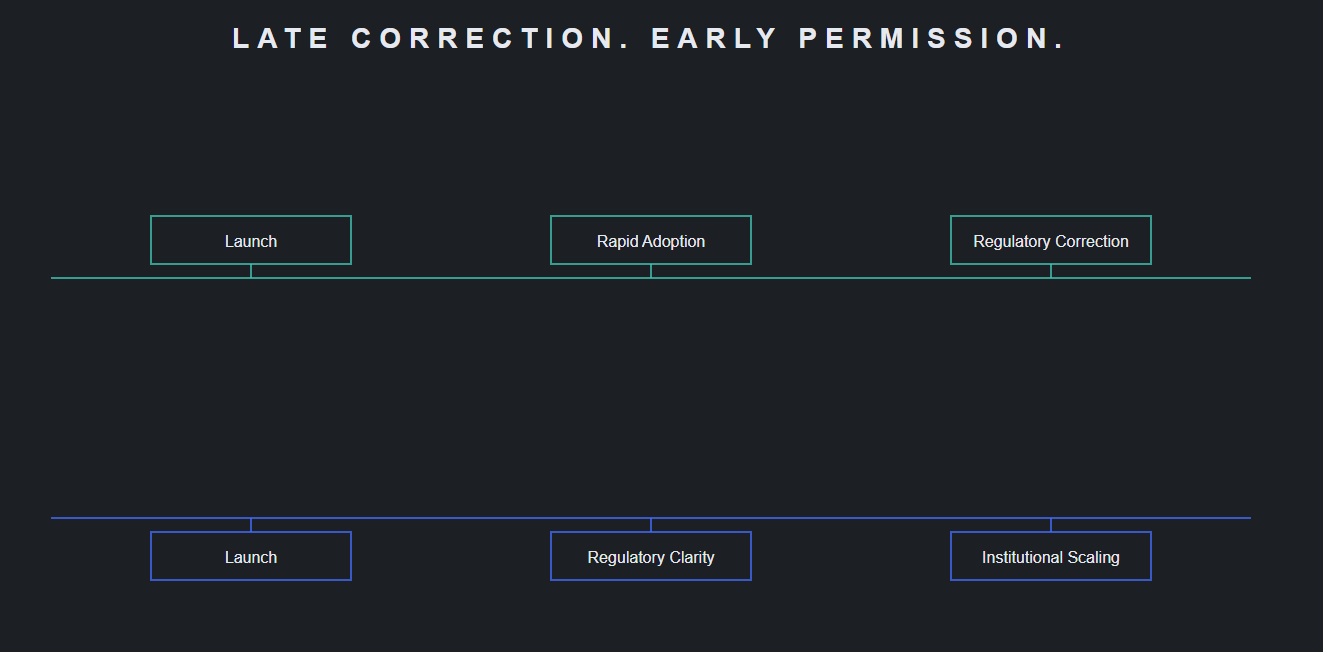

BNPL providers began operating in the mid-2000s. Peak merchant adoption occurred around 2018. Regulatory intervention followed between 2024 and 2026, nearly two decades after initial deployment. Regulation arrived as correction. Consumer protection frameworks addressed loan stacking, affordability assessments, and credit reporting gaps that had already become systemic.

The scale of accumulated risk became visible only in retrospect. By 2025, 42% of BNPL users had made at least one late payment, up from 39% in 2024 and 34% in 2023. Nearly a quarter of users reported having three or more active BNPL loans simultaneously. The CFPB found that 63% of borrowers originated multiple simultaneous loans at some point during the year, with 20% qualifying as heavy users. That’s more than one loan per month on average. Because most BNPL activity is not reported to credit bureaus, other lenders cannot see the full debt picture. The credit system is operating with incomplete information, creating what regulators call “phantom debt.”

Crypto infrastructure is experiencing the opposite sequencing. For years, regulatory ambiguity constrained institutional participation. Custody treatment under SEC Staff Accounting Bulletin 121 made balance sheet exposure economically unattractive. Banks holding crypto assets faced capital requirements that made custody services commercially unviable. Stablecoin issuance lacked statutory clarity. ETF access was blocked.

Between 2024 and 2025, these constraints shifted. Spot Bitcoin ETFs were approved in January 2024. SAB 121 was rescinded in January 2025, removing punitive custody accounting treatment and enabling banks to hold crypto assets without disproportionate capital charges. The GENIUS Act provided a federal framework for stablecoin issuance in mid-2025. MiCA came into force in Europe, establishing clear reserve requirements, transparency standards, and authorization pathways for stablecoin issuers.

The mechanical difference is significant. SAB 121 required banks to record customer crypto assets as liabilities on their own balance sheets, with corresponding asset recognition. This effectively treated custody as if the bank had borrowed the assets, triggering capital requirements that made custody economically irrational. The rescission returned crypto custody to the same accounting treatment as other custodial assets: off-balance-sheet, with fee income and no capital penalty.

The distinction is mechanical. BNPL regulation imposed new obligations after adoption saturated. Crypto regulation removed structural impediments during adoption acceleration. This distinction matters because permission unlocks balance-sheet activity, while restraint merely shapes behavior after activity is already unavoidable.

This sequencing explains why institutional adoption accelerated once guidance crystallized. When custody became balance-sheet neutral and stablecoins gained statutory recognition, infrastructure projects moved from exploratory to executable. In 2025, approximately 80% of surveyed jurisdictions saw financial institutions announce digital asset initiatives. The Basel Committee announced a review of its proposed prudential rules for banks’ crypto exposures, acknowledging that the original framework (which would have required full capital deductions for most crypto assets) was being reconsidered in light of market developments and the failure of major jurisdictions to adopt the standards as written.

Sequence, Not Sentiment.

Merchants adopted BNPL because the operational sequence was simple:

Integrate API.

Observe metrics.

Capture upside.

Offload risk.

Institutions adopt crypto infrastructure through a more constrained sequence.

Custody must be resolved before assets can be held. Accounting treatment must be clarified before exposure is economical. Compliance frameworks must integrate before transactions can scale. Settlement rails must interface with existing treasury systems before capital can move.

Each step introduces gating functions that slow deployment but increase durability. This explains why early crypto narratives focused on decentralization did not map to enterprise behavior. Institutions lacked key attributes that allowed blockchains to fit into existing control frameworks.

The sequence now exists in specific contexts. JPMorgan launched JPM Coin (JPMD) on Base, enabling institutional clients to send and receive tokenized deposits on a public blockchain with near-instant 24/7 settlement. B2C2, Coinbase, and Mastercard completed test transactions. The deposit token represents JPMorgan’s existing bank deposits on-chain, offering the regulatory compliance, KYC infrastructure, and banking integration that institutions require (combined with the speed, availability, and composability that public blockchain provides). DBS and Kinexys announced they are developing an interoperability framework to enable transfers of tokenized deposits across public and permissioned blockchain networks.

JPMorgan’s Kinexys platform has processed over $1.5 trillion in notional value to date, averaging more than $2 billion daily in transaction volume. Payment transactions on the platform have grown 10x year-over-year. The use cases include intraday repo transactions (more than $300 billion processed to date) where tokenized collateral enables short-term borrowing without the settlement friction that traps capital in traditional fixed income markets.

This is infrastructure deployment, not experimentation. However, it remains concentrated among specific institutions, specific use cases, and specific counterparty relationships. The lesson from BNPL is that adoption does not require belief. It requires workflow fit. The constraint for crypto is that workflow fit must be achieved at deeper layers of the stack, which takes longer and scales less visibly.

Checkout Firms Become Settlement Firms.

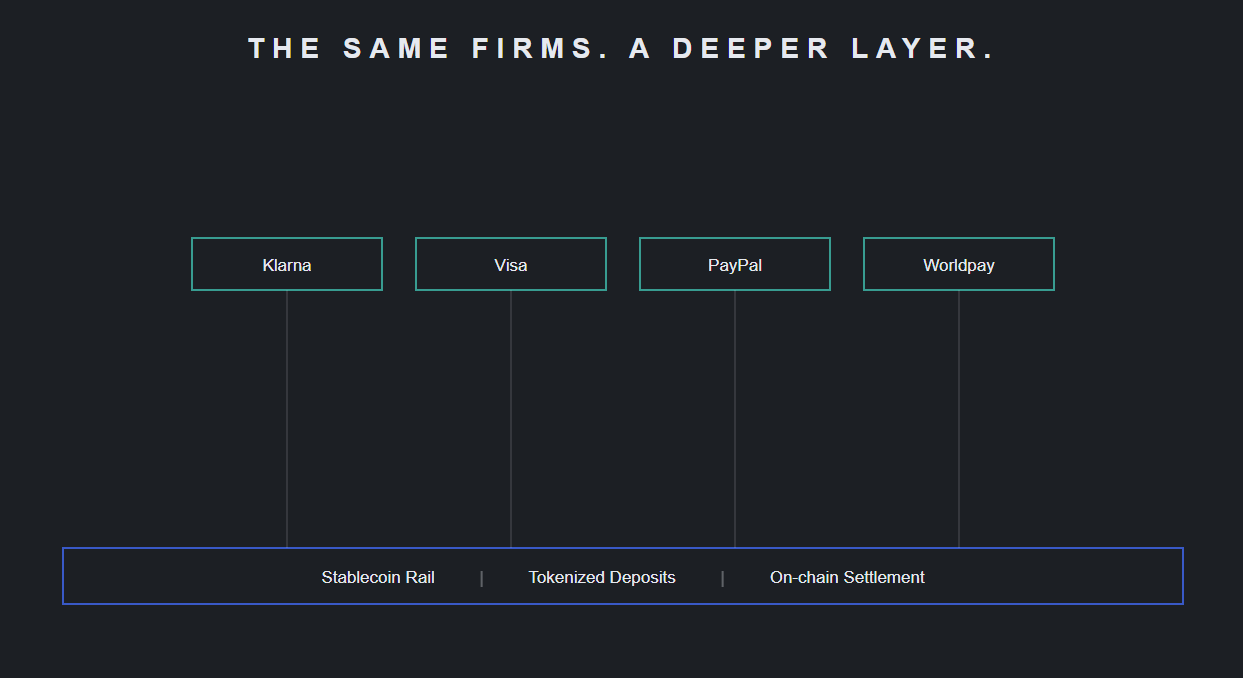

The BNPL-crypto comparison is not merely parallel. It is becoming sequential. The same operators who solved checkout friction are now adopting crypto infrastructure to solve their own settlement friction.

Klarna’s November 2025 launch of KlarnaUSD on Stripe’s Tempo blockchain represents the most visible convergence point. The driver is not consumer demand for “crypto BNPL” (which remains minimal) but merchant and institutional demand for faster settlement and lower cross-border fees. Klarna estimates $120 billion in annual cross-border transaction costs across its network. Stablecoin settlement reduces per-transaction costs to under $1. This represents orders-of-magnitude cost reduction at the settlement layer, and it is forcing adoption through the same mechanism that drove merchant BNPL integration. Executives have to acknowledge when measurable friction gets translated into recoverable margin.

The architecture is hybrid. Credit decisions remain off-chain: traditional underwriting, machine learning models, regulatory compliance. The consumer experience is unchanged. It’s still “Pay in 4,” instant approval, familiar repayment options, but the settlement layer is migrating on-chain. Merchants receive payouts in stablecoins within seconds, 24/7, rather than waiting two to three business days for correspondent banking settlement. The embedding depth distinction holds: BNPL operators are preserving the shallow integration layer (consumer-facing checkout) while replacing the deep layer (institutional settlement infrastructure).

Visa’s stablecoin settlement program reached $3.5 billion in annualized volume by late 2025, with USDC on Solana now live for U.S. issuer-acquirer settlement across 130+ stablecoin-linked card programs in 40 countries. Worldpay partnered with Fireblocks to enable instant USDC settlement for merchants globally. PayPal, which processed $33 billion in BNPL volume in 2024, is pursuing parallel stablecoin integration for cross-border merchant payouts.

The competitive logic is self-reinforcing. BNPL providers who move settlement on-chain reduce operational costs, improve cash flow through instant payout, and can offer lower merchant fees, allowing them to win market share from providers still operating on traditional rails. Providers who do not adopt face margin compression as competitors capture the efficiency gains. This mirrors the merchant-side BNPL adoption dynamic. Once competitors demonstrate measurable uplift, opting out becomes economically irrational.

The sequencing matters. Consumer-facing on-chain BNPL remains years away because wallet UX friction, regulatory complexity, and user education are still binding constraints. That said, B2B settlement infrastructure is deploying now. The current phase is institutional optimization, not consumer revolution. Consumers transact in familiar interfaces; BNPL providers and merchants capture the settlement efficiency invisibly. This is consistent with the embedding depth framework: deep infrastructure changes first, surface-level changes follow if/when the stack matures.

The convergence also validates the regulatory sequencing argument. Klarna’s KlarnaUSD operates under banking regulation as a stablecoin issuer, not consumer credit regulation as a payment mechanism. The GENIUS Act, SAB 121 rescission, and MiCA created the permission structure that enabled deployment. Regulation arrived before operational scaling, which is the inverse of traditional BNPL, where consumer protection frameworks addressed harms that had already accumulated. Whether this regulatory gap closes, and how quickly, will shape the next phase of convergence.

The Interoperability Constraint

BNPL succeeded in part because it layered onto existing payment rails without requiring coordination across competing systems. Merchants integrated a single API. Consumers used existing cards and bank accounts. The infrastructure was additive, not substitutive. No interoperability problem existed because BNPL providers did not need to coordinate with each other. They each plugged into the same underlying rails.

Interoperability is the BNPL-equivalent gating factor for crypto adoption.

Liquidity is currently fragmented across chains, protocols, and institutional ledgers. JPMorgan has its permissioned blockchain. Goldman Sachs has theirs. Public networks like Ethereum, Solana, and Base each host different assets and settlement systems. Klarna is building on Stripe’s Tempo. If a tokenized Treasury on a private bank ledger cannot interact seamlessly with a stablecoin on a public protocol, the efficiency gains remain siloed.

This fragmentation creates “walled gardens” of liquidity rather than a unified settlement layer. The efficiency gains that justify adoption at one institution may not compound across institutions if assets cannot move freely between systems. Without interoperability, crypto infrastructure risks a different kind of plateau than BNPL faced. It’s not risk from accumulation, but a failure of coordination.

BNPL’s gating factor (merchant integration) was primarily technical and commercial. Crypto’s gating factor is political, institutional, and regulatory as much as it is technical. Kinexys by JPMorgan recently completed a cross-chain delivery versus payment transaction with Chainlink and Ondo Finance, settling tokenized U.S. Treasuries against USD deposits across different blockchain networks. The transaction demonstrated that assets on a permissioned institutional ledger can interact with assets on a public blockchain through interoperability protocols, but it remains a proof of concept.

The pattern from BNPL suggests that adoption accelerates when integration complexity decreases. BNPL providers made integration trivially easy. Crypto infrastructure must do the same. The projects most likely to scale are those that abstract away chain-level complexity and present unified interfaces to treasury systems. The competition is not between blockchains. It is between interoperability frameworks that can deliver the seamlessness institutions require.

Delivering seamlessness requires agreement on standards, governance, and liability allocation across institutions that may be competitors. Unfortunately, this not a technical problem with an elegant solution. It is a coordination problem that requires institutional collaboration. How quickly that negotiation proceeds will determine whether crypto infrastructure adoption continues to accelerate or reaches an interoperability-constrained ceiling.

Where the Analogy Breaks.

A common objection to the views presented above is that BNPL rode consumer demand while crypto infrastructure lacks a comparable forcing function. Consumers demanded flexible payments. Institutions, critics argue, can tolerate settlement inefficiency indefinitely.

This underestimates competitive pressure inside institutional markets, but it does not entirely miss the mark. Settlement inefficiency manifests as higher funding costs, slower capital rotation, and increased counterparty exposure. These are not abstract costs. They appear in return on equity, liquidity ratios, and intraday credit usage. The BIS estimated that settlement failures and related penalties cost the global financial system approximately $915 billion annually. This figure makes the efficiency case concrete, though it represents system-wide costs rather than savings capturable by any single institution.

When one institution reduces settlement time from days to minutes, peers face visible disadvantages. Liquidity utilization improves. Balance sheet efficiency increases. Competitive benchmarks shift. This mirrors merchant behavior under BNPL adoption. Once competitors capture efficiency gains, opting out becomes harder to justify.

The BNPL-crypto convergence provides direct evidence. Klarna, Visa, PayPal, and Worldpay are not adopting stablecoin settlement because of ideological alignment. They are adopting it because they measured the friction, quantified the cost, and observed competitors moving. The forcing function is not consumer demand for crypto. It is institutional demand for settlement efficiency, expressed by the same operators who built their businesses on resolving consumer-facing friction.

The competitive dynamics are visible in announced initiatives. Visa is expanding stablecoin settlement “because our banking partners are not only asking about it—they’re preparing to use it.” Nine European banks announced plans for a euro-denominated stablecoin to support cross-border settlement inside the EU. Citigroup joined the consortium as well. The Federal Reserve published research modeling that even moderate stablecoin adoption could reduce bank lending capacity by $190–$408 billion as deposits migrate. That’s a figure that captures institutional attention regardless of ideological position.

The difference is timescale. Consumer feedback loops operate daily. Institutional feedback loops operate quarterly. The pressure is slower, less visible externally, and mediated by procurement cycles and risk committee approvals. Whether this pressure produces BNPL-like speed is uncertain. It will not produce BNPL-like visibility. What is clear is that the pressure exists and is being measured.

Failure Modes Reveal Where Risk Accumulates

BNPL’s failure mode emerged at the credit layer. Loan stacking increased. Subprime concentration rose. Late payment rates climbed to 42% by 2025. The share of users with subprime or deep subprime credit scores reached nearly two-thirds, with approval rates for these applicants at 78%. Regulatory correction targeted affordability and reporting, but it arrived after the risk had already accumulated across millions of loans outside the traditional credit visibility system.

Crypto infrastructure’s potential failure modes sit elsewhere, and governance is arriving during adoption rather than after it. This is the inverse of the BNPL pattern. It does not mean the risks are smaller or better managed. It means they accumulate in different places.

Custody concentration creates single points of operational risk. A small number of qualified custodians hold the majority of institutional crypto assets, concentrating exposure at individual firms. Stablecoin issuers introduce counterparty exposure. If users lose confidence in redemption, runs could trigger fire sales of reserve assets. The USDC depeg during the Silicon Valley Bank failure demonstrated this dynamic. When Circle disclosed deposits at SVB, USDC traded below par until confidence was restored.

Hybrid architectures introduce correlation risk. If a proprietary stablecoin such as KlarnaUSD experienced reserve stress, settlement disruptions could cascade to merchants dependent on instant payout. Concentration of settlement on a small number of stablecoin rails increases systemic correlation relative to distributed correspondent banking.

Interconnection with decentralized finance introduces additional tail-risk propagation channels. Fiat-backed stablecoins are structurally different from algorithmic designs, but interconnection creates transmission pathways that remain difficult to model in advance.

Cross-jurisdictional regulation creates fragmentation risk. Different frameworks in the US, EU, and Asia may limit interoperability or push activity into unevenly supervised venues. Klarna operates in 26 markets. Stablecoin settlement must navigate 26 regulatory regimes simultaneously.

Efficiency does not eliminate systemic exposure. It relocates it. Stablecoin adoption alters bank deposit composition and funding stability. Federal Reserve estimates suggest that moderate adoption could reduce bank lending capacity by between $190 billion and $408 billion, depending on migration intensity. On-chain settlement also compresses liquidity cycles. Liquidity moves faster. Redemption cycles shorten. Features that reduce settlement friction can increase propagation speed during stress.

These are not arguments that adoption will halt. They indicate where risk management must focus. Standardization is a coordination problem, not a technical inevitability. Common custody standards, reserve transparency requirements, and interoperable compliance frameworks require alignment among institutions with competing incentives and regulators with different mandates. The pace of that coordination will determine whether crypto infrastructure scales without accumulating fragility of the kind that eventually constrained BNPL.

The Metrics That Decide

BNPL adoption plateaued when the primary friction was resolved and secondary risks accumulated. Crypto infrastructure adoption is entering a different phase: primary frictions are being resolved at specific points while governance and risk management develop in parallel.

The metrics that matter are not token prices or consumer awareness. They are settlement duration, liquidity utilization, custody concentration ratios, and regulatory harmonization across jurisdictions. Where these metrics improve, adoption will continue. Where they degrade or fragment, constraints will emerge.

Current data points provide baseline visibility. Only 33.5% of cross-border payments currently settle within one hour which compares to a G20 target of 75% by 2027. Stablecoin market capitalization exceeded $316 billion in 2025, with monthly transaction volumes above $1.25 trillion. B2B stablecoin payment volumes reached an annualized run rate exceeding $120 billion. Visa’s stablecoin settlement reached $3.5 billion annualized. Kinexys processes over $2 billion daily. These figures establish the scale of activity shifting onto new rails, though they represent a small fraction of global settlement volume.

The BNPL-crypto convergence offers a leading indicator. If Klarna’s KlarnaUSD deployment scales successfully through 2026, if Visa’s stablecoin settlement volumes continue compounding, if competing BNPL providers adopt stablecoin rails to maintain margin parity, these are observable behaviors that validate the adoption logic. If interoperability remains fragmented, if regulatory arbitrage closes faster than infrastructure matures, if custody concentration creates settlement failures, then these are observable behaviors that indicate constraint.

BNPL’s history shows that financial innovation enters systems through measurable friction relief. Crypto infrastructure is following the same logic at a deeper layer of the stack. The BNPL operators who demonstrated this pattern are now extending it to their own settlement infrastructure. The adoption mechanism is analogous. The timeline, visibility, and constraint structure are not. The shift is operational, not conceptual, but it is also slower, less visible, and more dependent on institutional coordination than the BNPL comparison might initially suggest.

The convergence is not a prediction. It is observable today. What remains uncertain is pace, scale, and whether the coordination problems that define deep infrastructure adoption can be solved before fragmentation creates its own ceiling.