Balance Sheet Battleground

Why the next phase of crypto adoption will be defined by where liquidity sits.

The Infrastructure Mirage

For the better part of a decade, the global financial community has been transfixed by a fascination with “rails.” The discourse surrounding digital assets has focused almost exclusively on the mechanical throughput of blockchains, the cryptographic security of decentralized applications, and the theoretical elegance of smart contract logic. This was the Infrastructure Phase. An era defined by the building of “containers.” From 2020 to 2024, the industry frantically constructed the pipes, the vaults, and the gateways intended to modernize the movement of value. During this period, the development of cryptocurrency markets was overwhelmingly infrastructure-focused because participation was structurally impossible without it. We built enterprise-grade custody platforms, standardized exchange APIs, and on-chain compliance services to solve five critical gaps: custody, exchange, execution, stablecoin utility, and regulatory reporting.

However, the industry is now confronting a fundamental truth of financial history… infrastructure is a necessary precursor to activity, but balance sheets determine who captures the economics. The mere existence of a faster or more transparent rail does not, in itself, shift the gravitational center of a market. Infrastructure answers the mechanical question of how institutions can participate, but it remains agnostic on the far more consequential question of who captures the value. During the infrastructure-heavy years, the answer to the latter remained stubbornly traditional. Centralized market makers captured spreads, early holders captured appreciation, and validators earned transaction fees. What this phase notably failed to do was create new balance sheet structures that shifted where deposits must reside or fundamentally change the structure of credit creation.

A common counter-argument to this thesis posits that the “rails” are the primary driver of value because they lower the cost of entry, thereby democratizing finance and naturally shifting economic power to the edges. Proponents of this view argue that the technology itself (by being open-source and permissionless) is the transformative force. While this is a compelling narrative for the retail-driven “crypto-native” world, it fails the test of institutional reality. In sophisticated financial markets, cost efficiency is a secondary concern to capital efficiency and risk-adjusted yield. An institution does not move a billion dollars because the transaction fee is lower; it moves it because the balance sheet upon which that capital sits offers a superior return or more efficient collateral utility. Infrastructure is a commodity that enables entry; the balance sheet is the strategic asset that determines the winner of the interest rate spread.

Financial history repeatedly demonstrates that infrastructure does not determine market power. Balance sheets do. The rise of the Eurodollar market in the 1960s did not require new payment rails or financial technologies. It required only that dollar deposits migrate outside the United States banking system. Once those balance sheets moved, a parallel dollar system emerged, operating at scale and largely outside domestic regulatory control.

We are now transitioning into a new Institutional Balance Sheet Restructuring Phase, an era beginning in 2025 where the “battleground” has shifted from the protocol layer to the allocation of liquidity. The first phase was about building the stage; this next phase is about the movement of the audience and their capital. A treasurer evaluating where to park cash in 2024 could technically use mature custody infrastructure to hold USDC, but the economics favored traditional bank deposits which offered FDIC insurance and competitive rates. Infrastructure was ready, but balance sheets had not yet shifted. That repositioning is only now becoming possible as the regulatory landscape moves from the abstract world of policy design into the concrete reality of implementation.

The next phase of crypto adoption will not be determined by infrastructure. It will be determined by where balance sheets move.

The Implementation Gateway

For most of the past decade, institutional participation was not limited by a lack of imagination or technology, but by the structural impossibility of integrating digital assets into a regulated balance sheet. Institutions require more than just a functional wallet. Legal clarity, specific accounting treatments, and rigorous governance structures are minimum requirements. Without a recognized definition of “custody” or a clear path for compliance, the risk of “balance sheet contamination” was too high for any regulated entity to ignore. Large-scale adoption was held in a “waiting game” as banks and asset managers waited for a clear signal that they could deploy capital without incurring existential legal risk.

That era of policy debate has finally begun to sunset, replaced by a phase of operational implementation. The passage of the GENIUS Act in May 2025 served as the definitive catalyst, establishing a national regulatory framework for payment stablecoins and finally providing the legal mandate for balance sheet allocation. By providing a federal licensing process and requiring 100% reserve backing with government-approved instruments, the Act transformed digital assets from speculative novelties into recognized financial instruments. This shift was further cemented in August 2025 when the SEC concluded its long-standing investigation into the Aave protocol with no enforcement action, effectively removing the regulatory “overhang” that had previously paralyzed institutional DeFi participation.

The focus has now shifted to the regulators’ rulebooks. In February 2026, the Office of the Comptroller of the Currency (OCC) issued a comprehensive proposed rule implementing the GENIUS Act, establishing a framework for “Permitted Payment Stablecoin Issuers” (PPSIs). This move is significant because it provides the granular prudential standards (covering reserve composition, capital sufficiency, and operational resilience) that allow a Chief Risk Officer or an Asset-Liability Committee (ALCO) to sign off on a digital asset strategy. The passage of GENIUS has embedded blockchain regulation into the governance structures of the world’s largest financial institutions.

However, understanding why this shift is happening now also requires acknowledging the “balance sheet inertia” that defines institutional behavior. Banks operate under strict regulatory capital ratios where every dollar of risk-weighted assets must be backed by capital. If a bank loses deposits to a stablecoin, it must reduce its lending proportionally to maintain these ratios. It’s a painful and expensive contraction with knock-on effects across the economy. This explains why adoption has appeared slow. It takes six to eighteen months for full technological integration and even longer for the governance cycles of audit and board review to complete.

The current environment is one of “compounding acceleration.” As first-movers like JPMorgan, Citibank, and US Bancorp begin to launch stablecoin settlement initiatives, they’re sending a clear signal to the market that the risk of being first has been replaced by the risk of being last. We are seeing a competitive pressure phase where peer-bank participation reduces adoption risk for the entire sector. As these institutional constraints ease, the path is cleared for the migration of liquidity from legacy systems into the new, programmable containers of the digital age. This transition forces us to reconsider the very nature of where money lives, shifting our focus to the “containers” that will hold the next generation of global liquidity.

Where Liquidity Sits

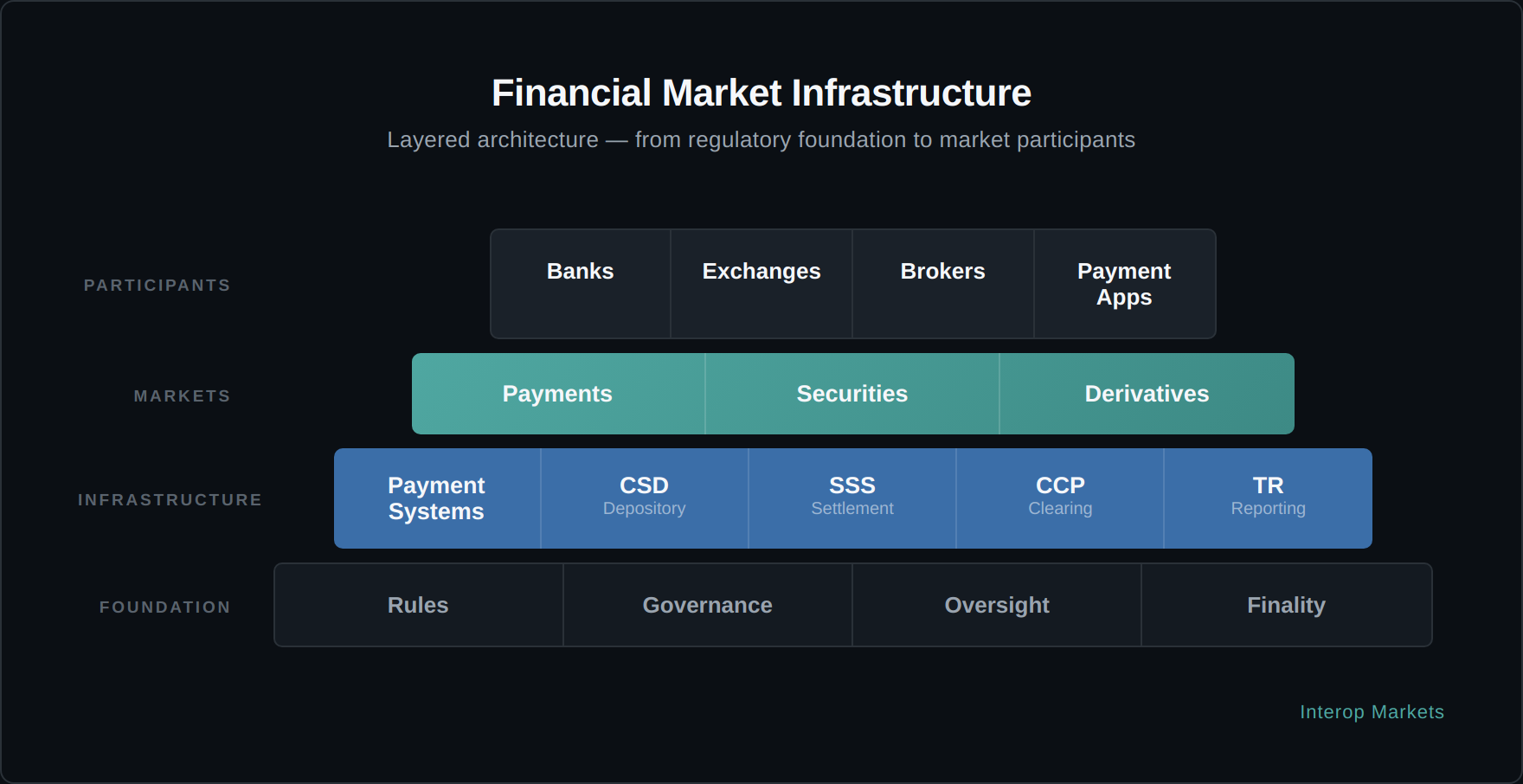

To grasp the magnitude of the shift currently underway, one must first appreciate the historical stability of financial “containers.” In every monetary era, liquidity must eventually find a home. It’s simply a function of technical storage, but satisfies the chronic global demand for safe, short-term assets. For centuries, this home was remarkably consolidated within a few well-defined structures: commercial bank balance sheets, central bank reserves, and money market funds. Each of these legacy containers functioned as an intermediary, capturing the economic value generated by the capital they housed.

The “Mathematics of Sitting” dictates that financial intermediation exists to solve a mismatch. Namely, that the world generates more cash from operations than it has immediate productive uses for, creating a permanent surplus of liquidity seeking safety. Traditionally, a commercial bank would capture this surplus as deposits, invest it in longer-dated assets like mortgages or corporate loans, and earn a substantial spread. This net interest margin (NIM) is the commercial and retail banker’s North Star. The bank’s shareholders are the primary beneficiaries of the “spread,” while the depositor receives a fraction of the yield in exchange for liquidity and government-backed insurance.

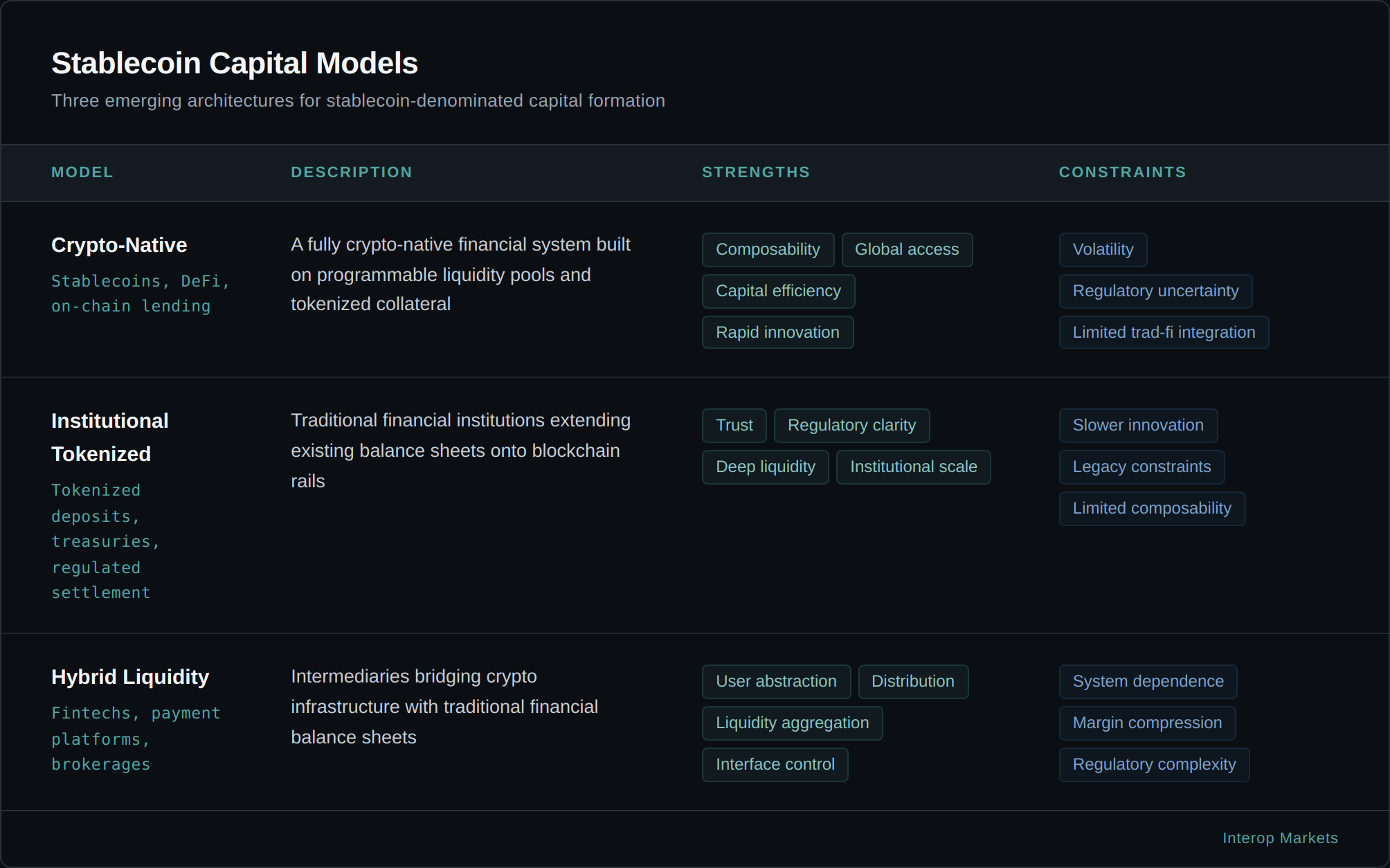

Digital asset infrastructure has introduced a new typology of “containers” that compete directly for this capital. These economic reconfigurations go beyond mere technological upgrades. When liquidity moves from a bank to a stablecoin reserve pool or a tokenized Treasury fund, the entity that captures the yield changes fundamentally. In a stablecoin reserve pool, for example, the issuer (such as Circle or Tether) earns the spread between the yield on the underlying Treasuries and the interest paid to the token holder, which is frequently zero. This effectively transfers the “economics of sitting” from the commercial banking sector to the digital asset issuer.

Furthermore, these new containers offer a degree of transparency and programmability that legacy structures cannot match. Tokenized Treasury funds, which reached a market value of over $11.5 billion in March 2026, represent a structural evolution where the yield of the underlying asset can accrue directly to the holder. This creates a powerful economic incentive. A sophisticated treasurer no longer has to choose between the safety of a bank and the yield of a fund; they can hold a tokenized fund that serves as both a yield-bearing asset and a high-velocity settlement medium. By redefining where liquidity sits, digital infrastructure is not just building new rails, it is creating a competitive market for the balance sheets that support the global economy.

Stablecoins Drive Relocation

Blockchain dollars represent the first large-scale migration of liquidity onto these new financial balance sheets, marking a transition from digital currency being a novelty to becoming a core component of financial plumbing. The stablecoin market sits near all-time highs at $311 billion, growing at an annual rate of 50-70%. This growth eliminates the notion that this is a speculative phenomenon. We are witnessing a tangible “dollar relocation” away from traditional banking infrastructure and into programmable settlement systems.

The economic impact of this migration is most visible through the lens of deposit substitution. When a corporation or an institutional investor moves $100 billion from a traditional bank deposit into a stablecoin container like USDC, the banking system experiences a profound loss of earnings power. In a traditional model, that $100 billion would support a bank’s ability to issue loans, earning the bank a net interest margin of roughly $3 billion annually. When that capital migrates to a stablecoin issuer’s reserve, those earnings are disintermediated. The bank loses the deposit, the ability to fund loans contracts, and the spread is instead captured by the stablecoin issuer.

This shift has profound implications for credit creation and financial stability. Research published by Federal Reserve economists in late 2025 emphasizes that high-adoption scenarios for stablecoins could lead to a bank deposit reduction ranging from $65 billion to $1.26 trillion. This reduction has the potential to reshape how credit is provided to the economy. Regional banks, which rely heavily on stable deposit bases to fund local lending, face the greatest vulnerability to this migration. As retail and corporate depositors seek the 24/7 settlement advantages of stablecoins, the traditional “float” that banks have long relied upon (earning spreads on in-transit payments) is rapidly becoming less compelling.

In response, the banking sector has moved from skepticism to a posture of participation. The announcements by JPMorgan, Citibank, and US Bancorp to launch their own stablecoin settlement infrastructures in late 2025 and early 2026 are not attempts to “disrupt” their own business, but rather to retain their importance as liquidity containers. These institutions recognize that the economics of the future favor the issuer of the digital container. By becoming issuers themselves, banks hope to capture the reserve yields that would otherwise flow to new entrants. Of course, this first great relocation of cash is only the opening act. As these new containers for liquidity stabilize, the focus of the battleground is shifting toward the more complex world of collateral and the leverage that powers global finance.

Programming Collateral

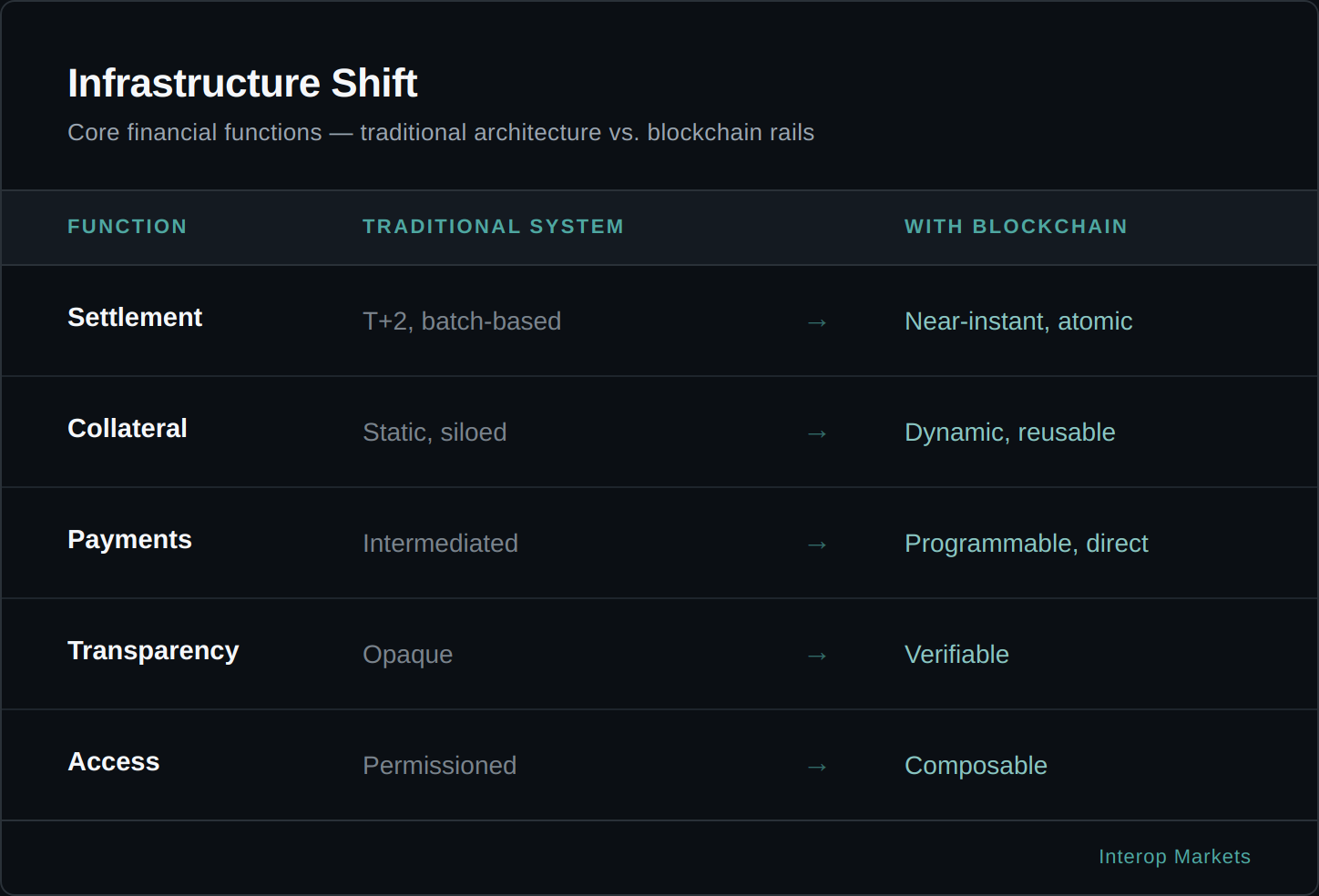

If the relocation of cash via stablecoins represents the first wave of this transformation, the migration of collateral represents a more fundamental restructuring of the financial system’s core leverage mechanics. Modern financial markets are essentially a vast network of collateralized obligations. The U.S. repo market alone, which facilitates the borrowing and lending of securities, moves between $2 trillion and $4 trillion… every day. However, this critical infrastructure remains burdened by the “discrete settlement windows” of traditional banking. In the current world, collateral moves only during banking hours, and custody fragmentation means that a security held at one bank cannot be instantly used to satisfy a margin requirement at another. This friction creates periods where capital is locked, unproductive, and unable to respond to real-time market volatility.

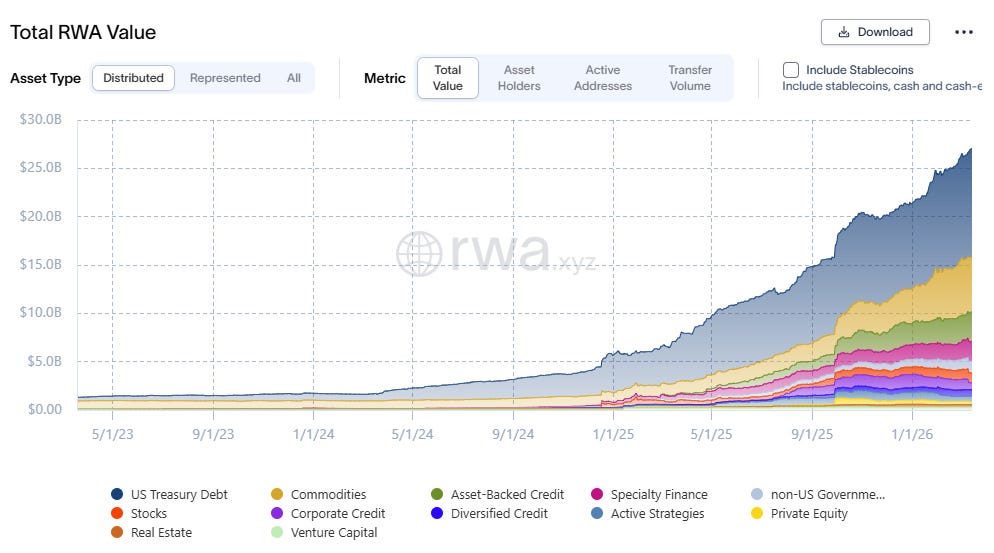

Tokenization transforms collateral from a static, location-bound asset into a programmable, high-velocity instrument. By converting U.S. Treasuries and other real-world assets (RWAs) into on-chain tokens, institutions gain the ability for 24/7 movement and atomic settlement. The growth of this market has been rapid; as of February 2026, the tokenized RWA market reached approximately $27.0 billion, with tokenized Treasuries accounting for roughly one third of that total. This surge is driven by institutional-grade products such as BlackRock’s BUIDL and Franklin Templeton’s BENJI, which allow holders to earn a 5% yield on underlying government securities while the tokens themselves remain mobile and deployable.

The true innovation lies in “collateral efficiency.” In a traditional repo transaction, an investor might be required to accept significant haircuts or face delays of several days to unlock and move securities between custodians. In contrast, tokenized collateral is “composable.” An institutional investor can hold $100 million in BUIDL tokens, deposit them into a protocol like Aave at a 95% loan-to-value (LTV) ratio, and instantly borrow stablecoins to fund a tactical opportunity. The collateral never leaves the digital environment, it is continuously re-valued by automated price feeds, and any margin calls are handled via instantaneous, automated liquidations.

This shift moves the “economics of the dealer” toward the “economics of the protocol.” In the traditional repo market, large dealer banks act as intermediaries, capturing a spread of roughly 50 basis points by borrowing at one rate and lending at another. In a tokenized ecosystem, collateral holders can self-match in DeFi lending markets, using software as an intermediary and capturing the full interest rate spread. We’re years away from seeing this at scale, but such a shift has the potential to move billions in annual earnings away from traditional dealer desks and toward protocol governance and asset holders.

To further appreciate the magnitude of the shift from cash to collateral, one must examine the institutional plumbing that has historically governed these movements. For decades, the global financial system has operated on a “T+X” settlement logic, where the “T” represents the transaction and the “X” represents a multi-day lag necessitated by manual reconciliation and inter-bank clearing cycles. In the traditional repo market, this delay acts as a silent tax on capital. When a dealer bank facilitates a repo, the collateral must be physically moved between custodians, often requiring human intervention to verify haircuts and legal titles. This creates a “liquidity moat” around the largest dealer banks, who derive their power not just from their balance sheets, but from their control over these proprietary settlement silos.

The mechanics of tokenized collateral dismantle this moat through atomic settlement. In a step-by-step institutional flow, the transition functions as follows:

Tokenization: A high-quality liquid asset (HQLA), such as a U.S. Treasury, is moved into a digital wrapper (e.g., BlackRock’s BUIDL), turning it into a 24/7 mobile token.

Instantaneous Posting: Instead of waiting for a Monday morning wire transfer, a treasury team can post this tokenized collateral to a lending protocol or a prime broker at 10 PM on a Sunday.

Real-Time Valuation: Smart contracts utilize decentralized oracles to mark the collateral to market every few seconds, rather than once per day, allowing for significantly higher loan-to-value (LTV) ratios because the risk of a “flash gap” in valuation is mitigated by continuous monitoring.

Yield Preservation: Crucially, the investor continues to earn the underlying Treasury yield while the asset is encumbered as collateral, creating a “yield-on-yield” opportunity that is operationally cumbersome in legacy systems.

For a corporate treasury team or an asset manager, this shift is a fundamental revaluation of their idle assets. In the traditional paradigm, a treasurer manages a “buffer” of cash that earns minimal interest simply to ensure they can meet sudden margin calls or operational needs. With tokenized collateral, that “buffer” can remain fully invested in yield-bearing Treasuries because the owner knows those assets can be converted to liquidity in seconds, not days. This removes the “liquidity discount” historically applied to long-term holdings.

For the banking sector, the implications are equally profound. Banks have long profited from the “float” and the intermediation spreads of the repo market. As collateral becomes programmable and self-matching, that toll evaporates. This is why the emergence of institutional “plumbing” like Anchorage’s Atlas network or JPMorgan’s internal tokenization efforts are so critical. They represent an attempt by financial institutions to build new silos before the old ones face competition. The transition from cash to collateral is the moment the financial system moves from a series of “discrete events” to a “continuous flow,” and the institutions that fail to adapt their balance sheets to this new velocity will find themselves holding increasingly static (and thus increasingly expensive) capital.

What appears to be an improvement in settlement speed is, in reality, a reconfiguration of how capital is deployed, valued, and intermediated.

The S-Curve of Adoption

The migration of institutional balance sheets is not a process of overnight disruption, but rather one of gradual absorption and eventual acceleration. It’s a “Web2.5” reality where blockchain technology is integrated into existing financial architecture rather than replacing it. Institutional adoption is currently being shaped by “balance sheet inertia,” a phenomenon where regulatory capital requirements, risk committee approvals, and legacy technology systems act as significant drag factors. Banks, for instance, cannot simply flip a switch to move assets. They must manage strict Tier 1 capital ratios and ensure that any move of deposits to a digital container does not force an expensive contraction of their lending books.

Despite these hurdles, the adoption of digital asset infrastructure is following a well-documented historical S-curve, similar to the multi-decade rollout of credit cards, the internet, etc.

Between 2015 and 2024, the market was in an “experimental” and “regulatory confusion” phase where growth was tempered by uncertainty. We have now entered the “Competitive Pressure Phase” (2025–2026), characterized by regulatory clarity and infrastructure standardization. During this phase, “You’re not the first, but you’re not the last” becomes the primary motivator for institutional treasurers. As more banks see their peers participating in stablecoin settlement or tokenized Treasury funds, the perceived risk of adoption drops precipitously.

The current scale of the market provides a baseline for a compounding acceleration. With Fireblocks securing over $5 trillion in annual digital asset transfers and institutional tokenized asset markets growing rapidly, the “plumbing” of the new system has reached production-grade readiness. This infrastructure standardization enables banks to build on proven systems rather than reinventing proprietary ones.

As we look toward 2027 and beyond, several “policy levers” remain that could further accelerate this migration. If stablecoin issuers were granted direct access to Federal Reserve Master Accounts, or if the current interest prohibition on payment stablecoins under the GENIUS Act were to be eased through affiliate “reward” structures, the flight of deposits from traditional bank ledgers to digital containers would likely accelerate meaningfully. The system is primed for a feedback loop where more stablecoin liquidity attracts more DeFi applications (likely permissioned), which in turn attracts more institutional capital, ultimately leading to a restructured financial landscape where the “battle for the rails” has been won, and the focus is entirely on the strategic management of the balance sheet.

The Winner of NIM

The transition from the Infrastructure Phase to the Balance Sheet Phase marks the moment when the “digital asset” conversation moves from the periphery of technology into the heart of global macroeconomics. For years, the industry operated under the assumption that building better rails would inevitably lead to a better system. We now understand that rails are merely the invitation. The transformation occurs only when the capital itself relocates. The “Battle for the Rails” has effectively been won by a standardized, institutional-grade stack of MPC custody, tokenized Treasury funds, and federally regulated stablecoin frameworks. The new battle (one that will define the next decade of finance) is for the balance sheets that hold the world’s liquidity and collateral.

Heading into the 2027–2030 horizon, the structural advantages will accrue to those who can most efficiently manage these new “digital containers.” We should expect a persistent compression of commercial bank net interest margins (NIM) as depositors increasingly prioritize the 24/7 settlement and higher utility of stablecoin-accessible yields. Large corporates and institutional investors will likely shift their primary savings and treasury functions toward DeFi and RWA markets, where the middleman’s spread is minimized by protocol transparency. This is not the end of the traditional bank, but it is the end of the bank as a static, unchallenged warehouse of cheap capital.

The winners in this new era will be the “Web2.5” hybrids, or institutions that recognize they are no longer just lenders, but managers of programmable liquidity. By 2030, when the stablecoin market is forecasted to approach $2 trillion, the distinction between “crypto” and “finance” will have largely evaporated. The system will have fully absorbed the efficiency of the rail into the stability of the balance sheet. In this restructured landscape, financial power will not belong to those with the most innovative technology, but to those who control the containers where the world’s liquidity and collateral ultimately sit. The battleground is set, and for the first time, the economics are up for grabs.

Crypto’s last decade was spent building infrastructure so institutions could participate. The next decade will determine where institutional balance sheets ultimately reside.