Becoming Invisible

Stablecoins, Distribution, and the Workflows Rewiring Finance

Structural transformations in financial architecture are rarely announced to the end user. They do not occur because a critical mass of individuals suddenly decides to abandon established habits in favor of superior cryptography or novel settlement mechanisms. Systems of exchange are deeply entrenched behavioral architectures. You cannot expect a corporate treasurer to manually manage private keys any more than you can expect a retail consumer to care about the routing protocols underlying a credit card transaction. True systemic change only occurs when new infrastructure is thoroughly absorbed into existing habits, familiar interfaces, and daily workflows. When financial evolution is successful, it is almost completely invisible to the people relying upon it.

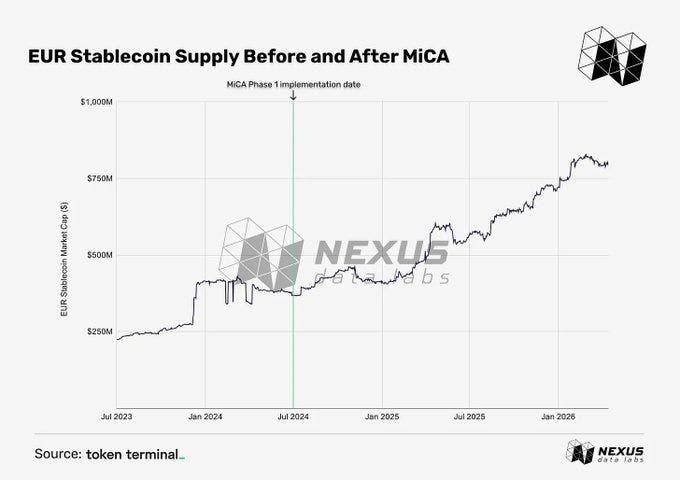

Over the past decade, market participants spent an extraordinary amount of capital and intellectual energy obsessing over the construction of new infrastructure. The collective focus rested heavily on block times, throughput capacity, protocol design, and the raw mechanics of distributed ledgers. That phase of foundational engineering has largely concluded. Stablecoin infrastructure has matured to a point of notable reliability. Simultaneously, comprehensive regulatory frameworks like the Markets in Crypto-Assets regulation in Europe and advancing legislative clarity in the United States have provided the legal foundation necessary for mainstream institutional capital to engage safely.

Because the infrastructure is now both technically functional and legally legible, the structural bottleneck has naturally shifted. The primary barrier to adoption has evolved into a matter of workflow integration. Industry focus has moved past initial ideological debates regarding decentralization, centering instead on strict operational requirements such as reconciliation, auditability, and settlement speed. Incumbents increasingly view stablecoins as backend settlement infrastructure capable of optimizing their own balance sheets and compressing transaction timelines.

As we have explored in prior installments of Interop Markets, value in financial services does not only accrue to the base layer rails. The contest for systemic power resides at the level of who commands liquidity, and distribution channels dictate where that liquidity flows. Stablecoins provide the most concrete and scaled arena where these theoretical frameworks manifest in commercial production. They are best understood not merely as a new asset class or a novel payment product, but as a highly efficient distribution technology. They are being woven into the checkout screens, treasury dashboards, and settlement environments that institutions and consumers already use.

The central thesis of the next financial epoch is clear: infrastructure lowers friction, distribution determines adoption, and workflow determines persistence. The market spent the last decade building the rails to lower friction. The years ahead will be shaped by who controls the distribution interfaces and the workflows where these programmable dollars are put to work.

The Limits of Supply Metrics and the Reality of Velocity

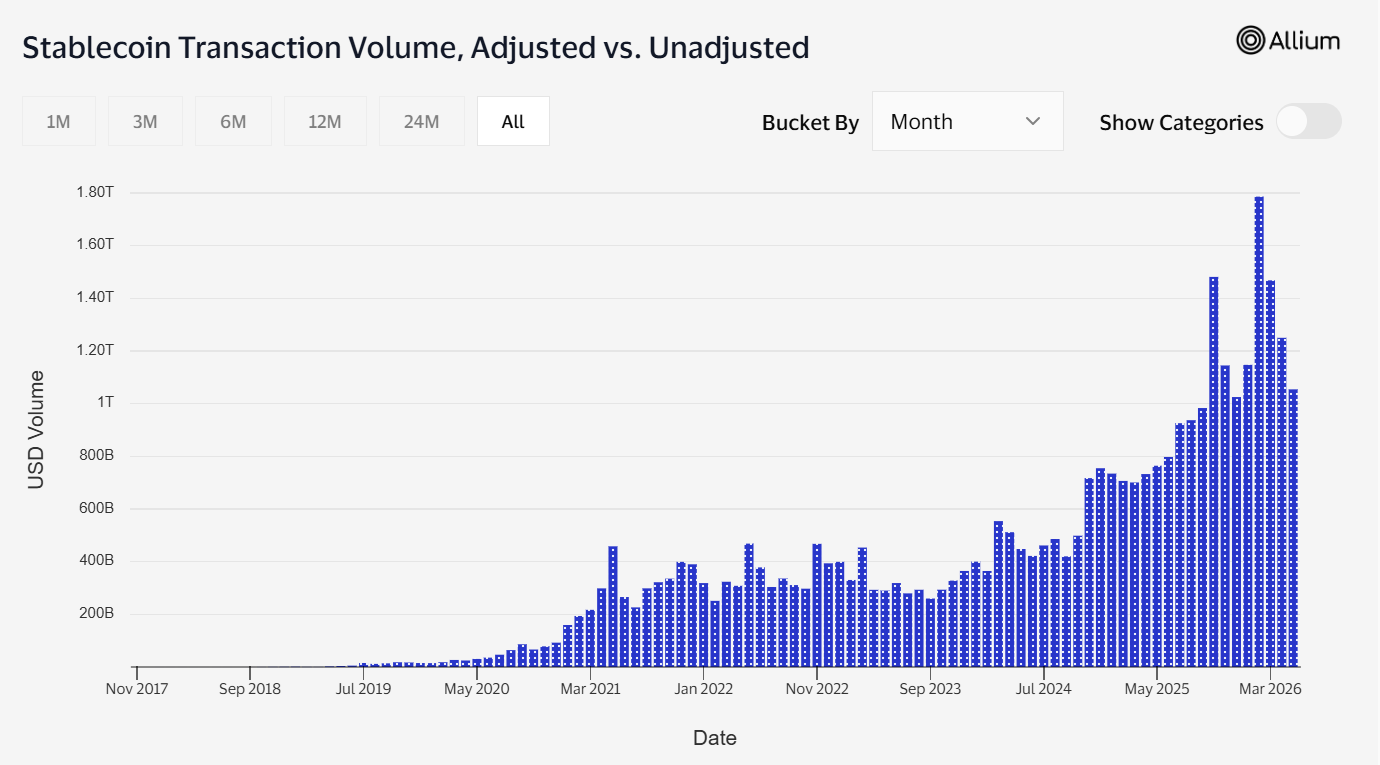

To grasp the magnitude of this transition, market observers must move beyond static metrics like total market capitalization. Simple supply metrics have historically served as an incomplete proxy for genuine economic adoption. Issuers can easily mint digital currency without securing structural distribution, leading to bloated figures that do not reflect actual commercial utility. Transfer volume, active user counts, and monetary velocity provide a far more accurate reflection of real economic penetration. When capital merely sits in a digital wallet, it functions as a speculative asset. When it moves continuously between counterparties to settle real economic obligations, it becomes true infrastructure.

Recent market intelligence illustrates this divergence clearly. Analysis from industry data providers indicates that stablecoins settled roughly ten trillion dollars in transactions over recent years, with a significant portion representing organic economic activity such as remittances, merchant payments, and non-automated exchange flows. By the latter half of the decade, that trajectory had steepened significantly. Independent analysis suggests that the aggregate stablecoin supply has climbed above 300 billion dollars, with on-chain transaction volumes measured in the tens of trillions. This volume routinely positions stablecoin transaction metrics as increasingly comparable to major global card networks.

The underlying rails are functional, operating at a scale commensurate with traditional global finance. As distributed ledgers prove their capacity to support global commerce, the industry’s focus has advanced toward where and how these digitized fiat flows are surfaced to the end user. This maturation signals a fundamental departure from the prevailing narratives of the past decade. Stablecoin expansion has broadened well beyond the localized dynamics of cryptocurrency market structure, increasingly resembling the historical evolution of digitized dollars. These assets are escaping the narrow confines of traditional banking constructs, only to be re-intermediated by whichever entity owns the default user interface.

The Segmentation of Settlement

The distinction between infrastructure and distribution explains a persistent market reality that confounds many institutional observers. The competitive dynamics between major stablecoin issuers are frequently misunderstood. Tether remains the dominant stablecoin by circulation and transactional share, even as alternatives like USDC, PYUSD, and bank-issued tokens gain favor with regulators and institutional allocators. Many analysts frame this dynamic as a technical or moral contest, assuming one model must eventually defeat the other. This framing is incorrect. Different distribution environments naturally produce different equilibrium states.

The distribution moat enjoyed by Tether is most visible in emerging markets, retail remittance corridors, and offshore trading venues. Networks like Tron have become the default cross-border settlement rails for small-ticket transactions, frequently processing transfers well under $1,000. In these specific environments, users require high-velocity, low-cost routing that does not rely on traditional Western correspondent banking chains. These flows are deeply concentrated across Asia, the Middle East, Africa, and Latin America, where formal banking access remains expensive or unavailable and informal foreign exchange channels dominate local economies.

Tether fulfills this demand because it achieved deep distribution within the specific digital wallets and informal networks these populations already utilize for daily trade. It dominates offshore and crypto-native corridors because it serves the specific workflow needs of those environments, commanding an approximate 60% market share of the circulating supply.

Conversely, the distribution footprint for USDC and its regulated peers represents a completely different market segment. Market commentators and institutional allocators consistently emphasize the tight reserve structures, audited backings, and strict regulatory alignments of these assets. This regulatory positioning has made them the preferred operational substrate for regulated platforms, compliance-focused decentralized finance protocols, and global card networks. Operating within strict permitted guidelines acts as a powerful distribution mechanism for Wall Street integration. It simplifies treasury routing, institutional settlement operations, and compliance sign-offs.

The resulting landscape is a profound market segmentation rather than a monolithic monopoly. Tether dominates high-velocity, emerging-market, and crypto-native corridors where informal distribution is paramount. Meanwhile, regulated assets like USDC, PayPal’s PYUSD, Ripple’s RLUSD, and tokenized bank deposits are better positioned as the default infrastructure for domestic card networks, financial technology payouts, and tokenized institutional funds. Both models thrive simultaneously because they have embedded themselves into fundamentally different workflows and distribution environments. The winner in any given corridor is simply the asset that integrates most seamlessly into the local interface.

Incumbents as Adaptive Distribution Networks

If the prior era was defined by the belief that decentralized protocols would outright replace established financial institutions, the current era is characterized by incumbents aggressively adopting these protocols to optimize their operations. Visa, Mastercard, Western Union, Stripe, PayPal, and Coinbase serve as premier case studies in how existing distribution monopolies adapt stablecoins to enhance their own architecture. They are not legacy institutions waiting to be disrupted by superior technology. They are highly adaptive distribution systems extending their reach onto new settlement rails.

Crucially, these incumbents are not attempting to teach their users how to interact with cryptography. They are absorbing stablecoin functionality into existing behaviors. Consumers still tap their physical cards. Merchants still check their balances in familiar digital dashboards. Remittance users still collect physical cash at local storefronts. The underlying settlement substrate changes, but the user behavior does not.

Consider the operational logic of the major card networks. Visa has been methodically expanding stablecoin settlement capabilities, allowing a curated set of clients to fulfill their settlement obligations using digital dollars rather than traditional banking rails. By expanding this settlement architecture across high-performance networks like Solana, Visa delivers continuous, seven-day settlement. This capability alters the mechanics of working capital. Traditional cross-border settlement often requires merchant acquirers and issuers to pre-fund accounts in local fiat currencies, trapping capital to account for the weekend delays and operating hours of the traditional banking system. By utilizing stablecoins as a backend routing mechanism, Visa compresses this latency, freeing up corporate working capital and improving its own internal efficiency.

Mastercard is pursuing a parallel strategy by partnering with financial institutions to deploy digital dollars issued under strict trust charters. By facilitating real-time card settlement through these regulated tokens, Mastercard demonstrates a definitive shift toward bank-ready infrastructure. The card networks are treating stablecoins as alternative backend routing mechanisms designed to bypass the friction of the correspondent banking system. Any sufficiently regulated stablecoin can sit behind the settlement corpus of a major payment network, but the economic rent remains firmly with the networks that own the merchant and the issuer relationships.

Western Union provides a compelling illustration of distribution leveraging new infrastructure to maintain its market position. The launch of a regulated payment token coupled with Western Union’s sprawling physical footprint of hundreds of thousands of agent locations across the globe creates a unique digital asset network with profound efficiency gains. It connects digital custodians directly to local cash payout infrastructure. A user can receive a digitized dollar abroad and cash it out at a local corner store without ever interacting with a traditional bank account or managing a private key. The defensive moat in this equation is not the blockchain itself; it is the last-mile physical access. No digitally native project has successfully replicated an equivalent physical cash-out network. The underlying token is highly interchangeable, provided Western Union remains the primary interface for the remitters and receivers orchestrating the transaction. By incorporating the new technology, they leverage their distribution to reap significant benefits.

“Today you can send money to any one of 191 countries pretty much in real time and you’re still able to do that. Um there is a lot of efficiency. So, if I can free up a couple billion dollars of capital, I can buy back half the company. Um, because we have cash sitting on the balance sheet to make all this thing work that all of a sudden I can get access to.”

— Devin McGranahan, President and CEO, Western Union

Internet-native payment platforms exhibit identical strategic integration. Stripe enables merchants to accept stablecoins directly at checkout, automatically converting the proceeds to fiat currency in the merchant’s balance. The merchant is never burdened with managing wallet security, sourcing liquidity, or understanding the underlying consensus mechanisms. They merely observe an additional tender type that settles faster and cheaper than traditional methods. Stripe sees so much potential in this that they build their own chain, embedding themselves deeper into customer wallets.

PayPal applies the same logic inside its consumer network. By deploying PYUSD as a fully backed stablecoin within PayPal and Venmo, it preserves familiar account and checkout flows while extending a cheaper funding rail into corridors where cross‑border transfer costs remain high. PYUSD can be used to fund Xoom remittances to roughly 160 countries with no Xoom transaction fees and is being rolled out across 70 markets, so users experience faster, lower cost transfers without changing how they initiate payments. Coinbase provides the institutional complement, using its exchange infrastructure and Prime APIs to let corporates and developers treat USDC as a native settlement and treasury asset, including programmatic USDC settlement on USD trading pairs with no added execution latency. In both cases, incumbent platforms are adopting stablecoins primarily as a way to improve settlement economics, funding flexibility, and operating hours inside existing products, rather than to introduce a visibly new financial behavior for end users.

Operational Permission: Treasury and Workflow Integration

While consumer payments and card settlement generate significant public visibility, the most significant migration is occurring deep within the less visible terrain of corporate treasury operations, enterprise resource planning systems, and institutional ledgers. This is the domain where workflow inertia is the strongest, where the cost of behavioral change is the highest, and where actual institutional capital resides. For institutional adoption to reach its full potential, it requires far more than technical capability. It requires operational permission. Institutional adoption is not about whether a stablecoin can move quickly from one digital wallet to another. It is about whether that transaction can be initiated, approved, reconciled, audited, risk-managed, and reported inside existing systems.

Corporate treasurers evaluate financial technology through the lens of practical utility, prioritizing the ability to seamlessly match an invoice against a purchase order inside a centralized software system. To be viable for a global corporation, a stablecoin transaction must fit within established policy bounds and submit to strict multi-signature approval processes. These movements of capital must also generate compliant account statements that feed directly into international financial reporting standard audits to avoid creating new administrative burdens. Stablecoins achieve their true institutional significance as they are absorbed into enterprise resource planning software and treasury management dashboards, demonstrating that the remaining friction in the market is fundamentally operational.

The integration of stablecoins into enterprise software ecosystems provides a foundational template for how operational permission is granted. Systems like the SAP Digital Currency Hub function as critical extensions connecting core enterprise resource planning systems directly to blockchain-based payment rails. Treasurers can select specific invoices, flag them for stablecoin settlement, and execute the payment using identical accounts payable processes that they would utilize for a traditional wire transfer. The software supports preconfigured integration for regulated tokens, presenting digital currency holdings within the exact same dashboard utilized for traditional fiat cash management.

Oracle applies a similar framework through its own blockchain platforms and specialized middleware providers. They position stablecoin payments as digital fiat rails that plug directly into corporate general ledgers. Orchestration layers automatically manage network fees, foreign exchange routing, and journal entries behind the scenes. This solves one of the most acute pain points in corporate finance. Traditional correspondent banking requires manual reconciliation of fragmented data across multiple institutions. By matching on-chain settlement events to accounting entries in real time, these software systems significantly reduce the burden of month-end reconciliation. Once embedded directly into an enterprise resource planning workflow, a stablecoin ceases to be perceived as a speculative digital asset. It is transformed into a mundane, highly efficient operational tool.

In the realm of institutional portfolio management, entities like BlackRock and Fidelity are building analogous workflow moats. BlackRock’s tokenized BUIDL fund scales into a multi-billion dollar asset by offering daily on-chain dividends, acting as a foundational collateral layer for other financial protocols. These asset managers effectively transform their funds into base layer infrastructure while retaining total ownership of the portfolio management interface. Fidelity similarly provides institutional-grade digital dollars designed to help portfolio managers deploy idle cash into on-chain liquidity products without ever leaving a secure operational framework. In all of these institutional examples, the technology only matters because it is subservient to the workflow. The user is granted the benefits of cryptographic settlement strictly through the permissioned lens of the software they already know how to operate.

Historical Precedents of Workflow Dominance

To comprehend the future trajectory of stablecoins, we must examine historical instances where interface and workflow ownership captured the majority of economic value. The patterns of financial history are remarkably consistent.

The proliferation of money market mutual funds in the late twentieth century serves as a compelling precedent. During a period of rising inflation, traditional bank deposits were artificially constrained by federal regulations. Money market funds emerged to offer market-clearing yields on cash equivalents. However, the structural inflection point did not occur upon the mere invention of the instrument itself. The true revolution materialized when major brokerages launched centralized cash management accounts. These products automatically swept idle balances into high-yield money market funds while simultaneously providing clients with check-writing capabilities and payment cards. Distribution and automatic sweeping made the complexity invisible. Corporate treasurers utilizing integrated enterprise software today will treat their choice of underlying stablecoin with a similar functional indifference.

The development of the Eurodollar market reinforces this macro pattern. Offshore dollar deposits flourished not because they relied on novel technology, but because global banks in London possessed the distribution capability to intermediate international trade outside the constraints of domestic regulations. Corporate treasurers and central banks accessed these offshore dollars through their pre-existing correspondent banking relationships. Overnight Eurodollar volumes ultimately eclipsed domestic federal funds volumes by vast multiples, yet the entire system remained invisible to the end user. Corporations wired funds and maintained deposits without concern for the specific jurisdiction where the ledger entry was booked. As major banks and payment networks continue to internalize stablecoins, this trajectory of invisible, large-scale settlement tends to replicate itself.

The dominance of information systems like the Bloomberg Terminal and operating platforms like BlackRock’s Aladdin highlights the formidable moat of workflow ownership in institutional finance. These systems evolved into ubiquitous monopolies by consolidating analytics, order management, compliance, and risk into unified daily terminals. Their enduring strength does not derive from proprietary data feeds, which are largely commoditized across the industry. Their strength derives from owning the end-to-end interface where capital allocation decisions are ultimately finalized and recorded.

Beyond the boundaries of pure finance, the structural competition between major mobile operating systems demonstrates how distribution strategies dictate economic outcomes regardless of technological parity. Open distribution models may capture the majority of global market share, but vertically integrated ecosystems consistently capture a vastly disproportionate share of total operating profits. By controlling the interface, defining the default user experiences, and securing the distribution choke point, platform owners maintain pricing power. This dynamic shows that economic rent accumulates around daily workflows instead of technical standards. The winning layer is consistently the one that owns the interface or the default behavior.

When applied to the institutional integration of stablecoins, these precedents provide a clear roadmap. Once digital dollars are fully integrated into global card networks, treasury management systems, and institutional portfolio platforms, the marginal blockchain network or token issuer will resemble an undifferentiated money market fund sitting behind a brokerage sweep account. The actual commercial moats will be built out of compliance workflows, automated approval chains, and unified software interfaces.

The Inevitability of Invisible Migrations

The current narrative surrounding digital assets often misprices the realities of commercial integration. A pervasive misconception assumes that legacy intermediaries will be structurally hollowed out by decentralized networks. The reality is that major payment networks, enterprise software providers, and federally chartered institutions are acting aggressively to embed new routing directly into their existing architecture. Rather than being displaced, these incumbents are positioning themselves as the primary distributors of tokenized dollars to the global corporate sector. The meaningful metric for capital allocators is not which token will achieve the largest static supply, but which interface will seamlessly capture the highest velocity flows within established user behaviors. The boundary between cash, collateral, and payment assets is rapidly dissolving inside automated institutional workflows.

The stablecoin migration will ultimately manifest as a faster checkout, a cheaper remittance, a cleaner reconciliation process, and a treasury dashboard that suddenly settles globally after hours. End users will experience their familiar financial architecture seamlessly evolving to become more liquid, programmable, and continuous. Capital will continue to pool where it is most easily managed, and the entities that command the screen will continue to dictate the terms of the flow.