How Financial Systems Become Fluid

Reflections on Building a Bridge Between Traditional and Blockchain Markets

The evolution of financial infrastructure is rarely as clean as the market narratives that surround it. More often, it is the slow recognition that the previous set of assumptions no longer holds. As the digital asset industry matures, the conversation around decentralized finance has shifted away from narrative momentum toward a quieter interrogation of what has actually been built. The defining feature of financial markets today is not speed, but friction. More specifically, viscosity.

In fluid dynamics, viscosity measures a substance’s resistance to flow. In financial systems, it manifests as institutional inertia, compliance requirements, and embedded behavior. A foundational mistake of early blockchain finance was assuming that technical superiority would compel adoption. Financial systems do not evolve through technical elegance; they evolve through workflow compatibility.

The Viscosity of Financial Systems

This friction is rarely an accidental byproduct of legacy technology. In traditional finance it is often embedded by design. Layered controls, capital standards, and operational committees ensure that critical functions continue through periods of stress. What appears externally as bureaucracy is internally treated as the rational stewardship of client assets and institutional reputation.

The design philosophy is, by necessity, stability-first. Product building is a gated process where features are constrained by custody rules and reporting standards. Execution slows, but durability becomes a feature rather than a later patch. When failure occurs, it rarely looks like sudden collapse; it appears as integration drag and an underreaction to change.

Crypto-native markets developed under different assumptions. Friction was minimized to accelerate experimentation, deployment, and global scaling. Permissionless deployment and token incentives allowed capital to move with extraordinary speed, often without the same operational safeguards. Building happened at the market edge, where products found demand quickly but frequently left users as the first live testers of the code and incentive design.

The result was a complementary tension rather than a clean opposition. Traditional finance favored predictability at the expense of execution speed. Crypto-native systems accepted breakage because iteration was the primary source of competitive advantage. The reflexive nature of low-viscosity markets, however, meant that liquidity could unwind as quickly as it accumulated, producing rapid contagion when stress arrived.

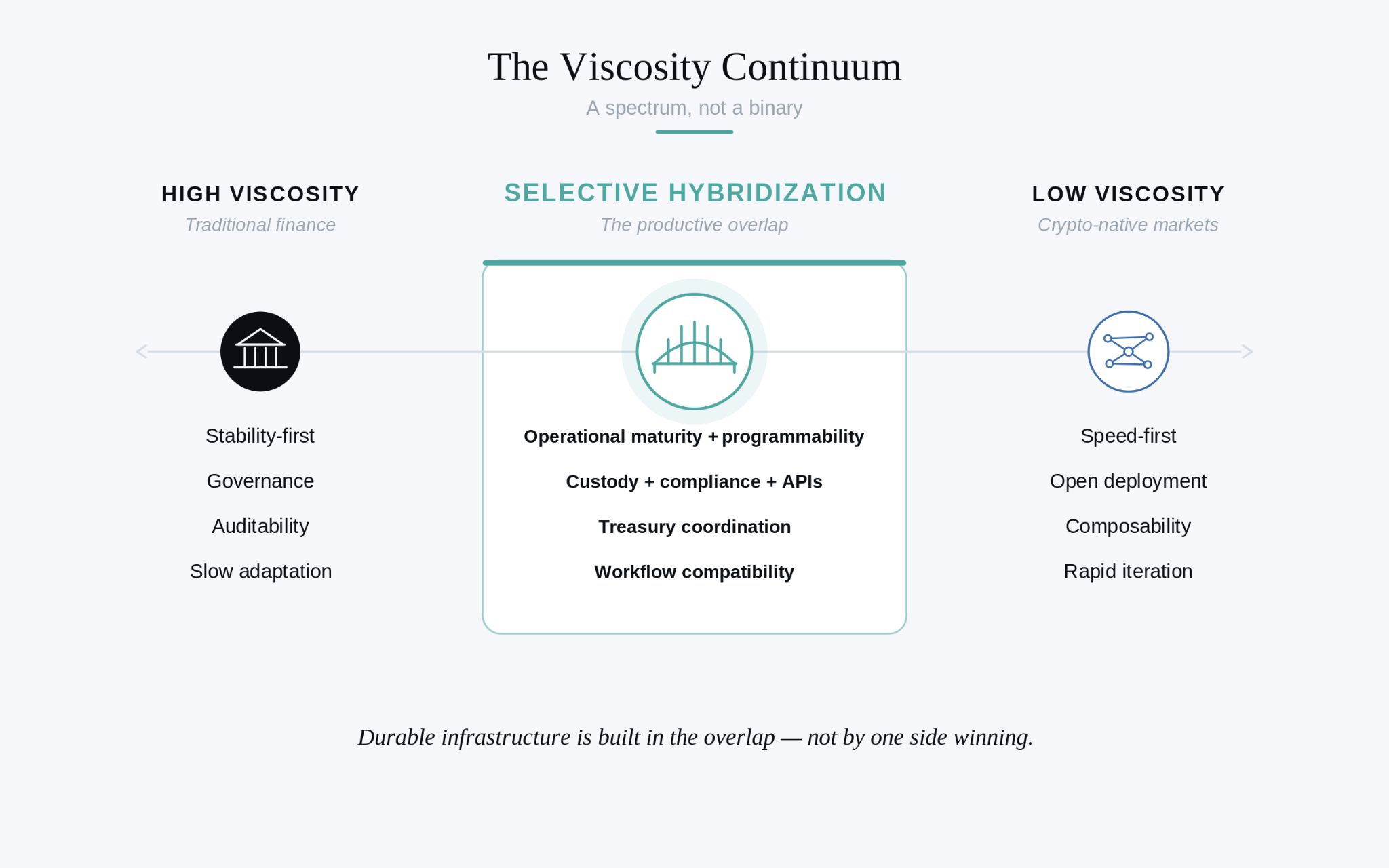

Expectations have shifted as the industry has matured. Crypto-native capital has begun demanding institutional characteristics: transparency, risk management, professional treasury oversight. A meaningful middle ground has formed, where participants operate on blockchain rails but expect the operational rigor of a more established system.

Selective Hybridization

The two systems are gradually converging. Crypto infrastructure is becoming more viscous in the areas essential for institutional scale: custody, compliance, risk management. Traditional institutions are modernizing delivery and reducing integration friction through APIs and programmable settlement systems.

The most durable infrastructure will combine the iteration speed of digital assets with the control architecture traditional finance spent decades refining. The challenge for institutions is rarely awareness; it is integration. Replacing treasury systems and reporting structures creates enormous organizational friction, and continuity remains a priority over optimization. The winners will be those who become embedded within existing workflows, turning integration from organizational surgery into a more incremental transition.

The reflections below are drawn from firsthand experience of this structural maturation, building an on-chain treasury management solution called Elara. They are an analysis of why infrastructure sequencing has inverted, and how we are designing systems for the eventual convergence of these two worlds.

The End of Narrative-Led Infrastructure

Joining the board of TrueFi offered a firsthand view of a market undergoing a profound structural repricing. The platform operated primarily as a credit marketplace for Real World Assets (RWAs), but the assumptions supporting the industry’s earlier expansion had clearly lost weight. My background in traditional finance suggested the core challenge of credit remained intact: bringing a loan on-chain does not solve counterparty risk.

Blockchains offer transparency, automated disbursements, and contingent payments, but they do not improve the underlying economics of a loan or the creditworthiness of a borrower. In a competitive environment where platforms fought over the same limited pool of high-quality credit, margins compressed and losses compounded. Many early operators tried to bridge the gap with unsustainable token emissions, a strategy with a visible ceiling.

The Strategic Pivot

If digital asset credit markets were going to mature, they would need more than isolated lending infrastructure. They would need treasury infrastructure capable of coordinating liquidity, collateral, settlement, and capital movement across increasingly interconnected on-chain environments. That realization pushed us from standalone products toward financial architecture.

Programmable treasury systems could eventually create tighter integration between liquidity management, collateral coordination, and credit formation in digitally native markets. Not because every component needed to sit inside a closed ecosystem, but because fragmented infrastructure produces operational drag, capital inefficiency, and counterparty complexity.

The long-term opportunity was never simply originating loans. It was participating in the broader coordination layer surrounding digital capital: treasury management, collateral mobility, liquidity routing, settlement infrastructure, and risk-adjusted capital deployment. The boundaries between treasury, settlement, and credit systems are becoming increasingly porous. Capital is starting to move through these environments less like isolated products and more like interconnected operational infrastructure.

Embedded in this shift was a practical economic point. Sustainable financial infrastructure cannot rely indefinitely on token emissions or incentive programs. Those mechanisms can accelerate early adoption, but they rarely produce durable economics on their own. A more resilient model comes from participating across multiple layers of the capital stack. Building infrastructure that sits close to treasury coordination, liquidity management, and collateral movement allows for economics that compound the way real financial systems do.

Programmable Treasury Infrastructure

Our focus moved toward stablecoins and treasury infrastructure, which had stopped being trading instruments or temporary exits from volatility. They had become foundational settlement rails for a new class of digitally native capital. That shift changes the nature of the problem. Once digital dollars function as treasury primitives rather than speculative tools, the operational requirements grow substantially. The challenge is beyond generating yield; we need to juggle liquidity, reporting, custody, and risk-adjusted returns across fragmented environments.

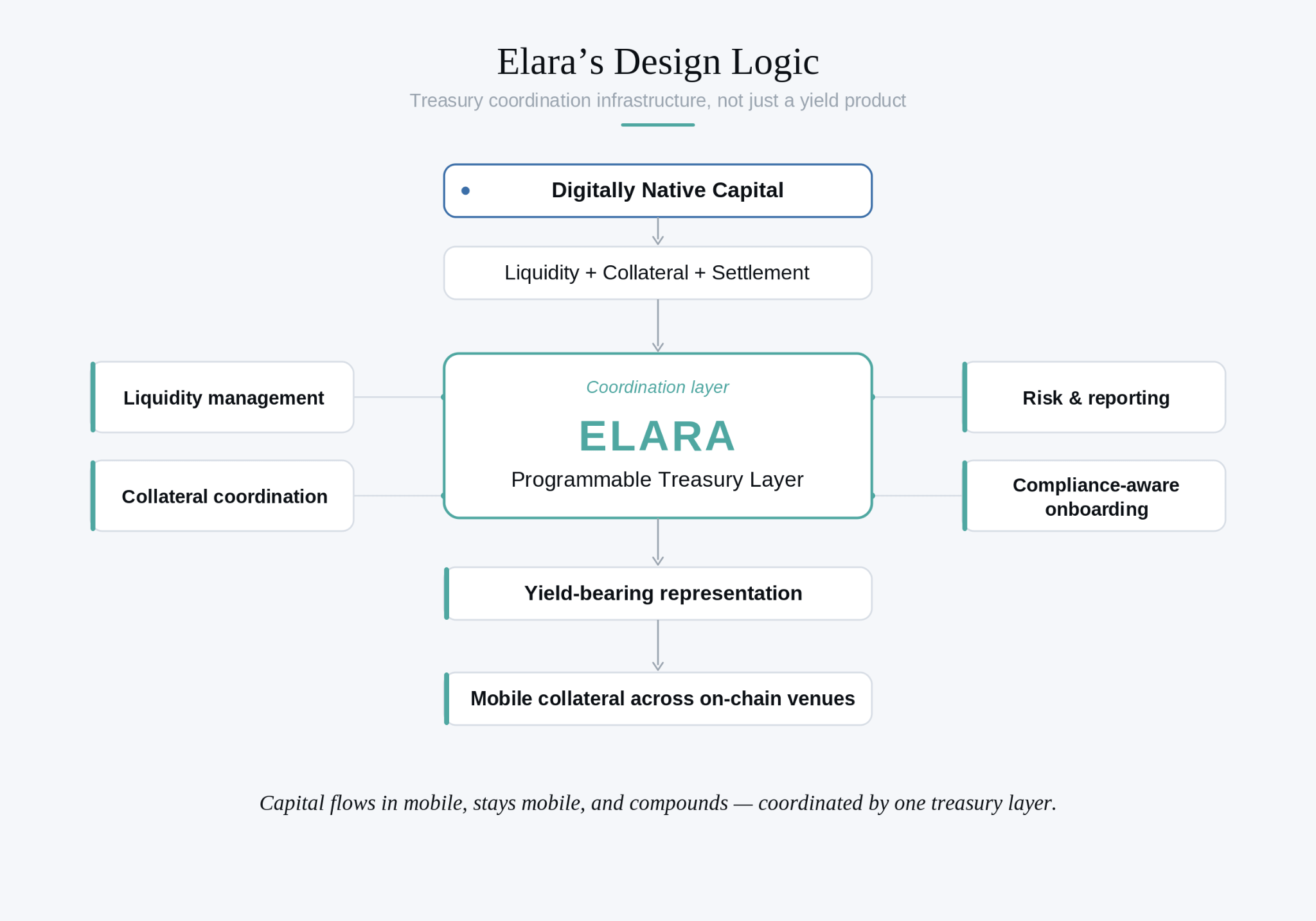

We wanted to build a dollar-linked collateral and treasury asset native to this ecosystem. Not another on-chain instrument, but infrastructure designed around capital efficiency, programmability, and operational flexibility. These ideas ultimately led to Elara.

One of the more consequential architectural decisions was separating liquidity from yield generation. Traditional fixed income products distribute yield through periodic cash flows. In programmable environments, value accrual can behave differently. Rather than forcing holders to sacrifice mobility to access yield, Elara was designed so that users could deposit the base asset and receive a freely transferable yield-bearing representation in return.

The distinction is subtle but operationally meaningful. As capital markets become increasingly digital and interoperable, the ability for collateral to remain mobile while compounding introduces a different treasury dynamic. Capital continues functioning inside broader on-chain systems rather than becoming static once deployed into a yield product. The staked representation compounds programmatically while remaining integrated with digitally native liquidity and collateral venues.

When such assets are used within credit markets, the result is notable. Collateral is no longer necessarily idle during the life of a loan. The underlying yield can partially offset financing costs, producing a more capital-efficient relationship between treasury management and credit formation.

Elara’s architecture reflects our broader thesis. Traditional financial operators are increasingly drawn toward blockchain systems not because existing products become obsolete, but because programmable infrastructure expands what those products can become. Static instruments begin functioning more like coordinated software: composable, interoperable, and continuously integrated with broader liquidity and settlement environments.

None of this removes the realities of operating inside digitally native markets. These environments remain faster, more fragmented, and structurally more reflexive than traditional fixed-income systems. Liquidity conditions can shift rapidly. Strategies involving market-making, treasury coordination, and on-chain liquidity management continue to carry execution risk, smart contract exposure, and operational complexity. Elara does not pretend blockchain-based infrastructure behaves like traditional finance. The objective is closer to the opposite: to acknowledge the nature of low-viscosity digital markets and introduce greater discipline into how capital moves through them. Programmable infrastructure does not eliminate financial risk. As digitally native capital markets mature, the operational architecture surrounding those risks becomes part of the product itself.

Liquidity as Infrastructure

At a practical level, the underlying strategy centers on market-making and liquidity provision for stablecoin pairs across decentralized financial markets. As stablecoin usage expands across trading, payments, collateral, and treasury management, liquidity coordination becomes an increasingly important financial function. Fragmented liquidity environments create demand for active capital deployment, spread capture, rebalancing, and continuous treasury management across on-chain venues.

The resulting yield emerges from real market structure dynamics inside digitally native capital markets: trading activity, liquidity fragmentation, volatility, and the operational complexity of maintaining efficient settlement. Unlike many reflexive crypto yield structures from earlier cycles, these opportunities do not depend on leverage to generate economic activity.

These environments remain structurally distinct from traditional fixed-income markets. Returns are influenced by liquidity conditions, execution quality, volatility regimes, smart contract risk, and broader market participation. When trading activity contracts or liquidity compresses, opportunity sets can narrow materially. During stress, treasury coordination and risk management become more important still. The pattern reinforces a broader thesis: economics increasingly accrue not to reflexive token incentive structures, but to disciplined treasury management and infrastructure capable of coordinating capital efficiently through changing conditions.

Funding the Vision

The initial instinct, shaped by the fundraising dynamics of the previous cycle, was to raise capital around the vision itself. Early discussions focused on the scale of the opportunity: digital dollar infrastructure, programmable treasury systems, and the long-term convergence of traditional finance with blockchain-based settlement rails.

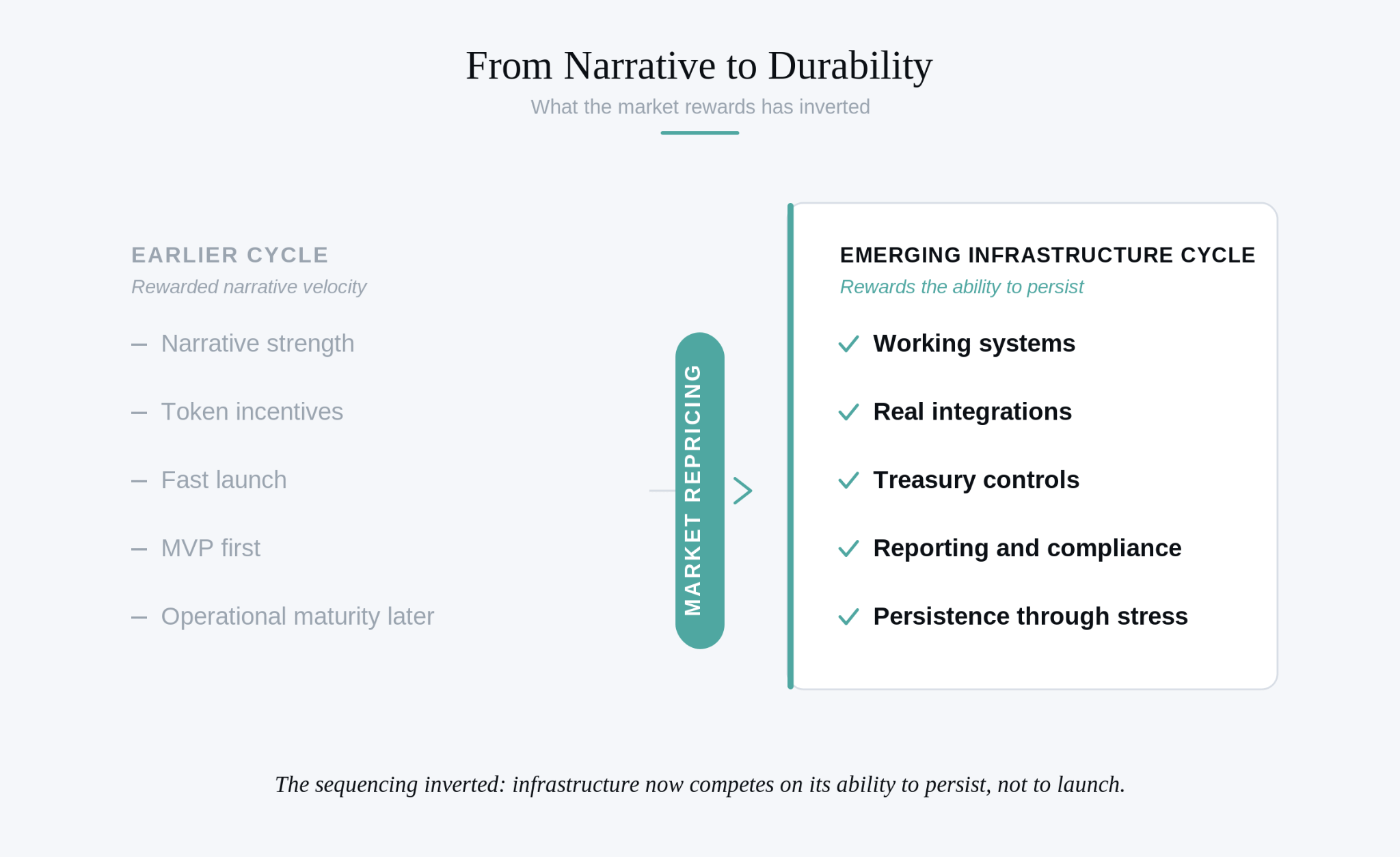

A few years earlier, that approach might have worked. Crypto markets had spent much of the prior cycle rewarding narrative velocity, where strong theses and token models could attract significant capital before infrastructure had matured. The environment had already shifted by the time we entered the conversation.

Members of the executive team engaged potential investors before meaningful infrastructure had been built, assuming the strength of the idea would carry the conversation. Instead, the conversations turned operational. Investors wanted functioning systems, integrations, reporting structures, treasury controls, counterparties, compliance frameworks, and evidence that the infrastructure could operate under real market conditions.

The shift was both inevitable and healthy. It reflected the lessons of the previous cycle, when markets became less willing to finance abstraction after watching loosely constructed systems unravel under stress. Technology accelerated the shift. As AI-assisted software development advanced, the scarcity value of early-stage code began collapsing. MVPs became easier to build, interfaces easier to replicate, and infrastructure more accessible. As software became commoditized, operational trust became more valuable.

The competitive advantage moved from who could tell the most compelling story to who could build systems capable of persisting through real market conditions. The sequencing had inverted. Earlier cycles rewarded teams for launching quickly and operationalizing later. The emerging market rewards the opposite: infrastructure businesses now compete on their ability to persist rather than their ability to launch.

Strength in Numbers

These realizations forced a deeper interrogation of why institutional adoption across digital assets has moved more slowly than many early builders expected, returning us to viscosity.

Banks, corporate treasuries, asset managers, and institutional allocators move slowly for rational reasons. Their operating models are built around continuity, auditability, risk containment, and procedural trust accumulated over decades. Reporting standards, investment committees, custody frameworks, and compliance processes exist to reduce the probability of uncontrolled failure when managing large pools of capital. What appears externally as friction is, internally, the infrastructure itself.

Crypto-native systems evolved around different assumptions. Capital mobility, composability, rapid iteration, and open deployment let blockchain infrastructure scale quickly across global markets. The advantage is adaptability. The weakness is that speed can outpace operational hardening, as the previous cycle demonstrated when liquidity, incentives, governance, and risk became increasingly intertwined.

The long-term capital base likely to move on-chain will remain high-viscosity in character, even as the underlying settlement infrastructure becomes more programmable. That recognition shaped Elara. Building purely for speculative velocity was unattractive; waiting for large institutional allocators to fully migrate on-chain before building anything was impractical. The realistic path was to build for the digitally native capital already in these markets while embedding the operational values institutional participants would eventually require.

In practice, that meant designing for treasury discipline, reporting awareness, and durability from the beginning rather than treating those features as later upgrades. The partnership with ArkenYield reflects the same philosophy. At its core sits a tokenized market-making and treasury strategy operating inside low-viscosity digital markets while incorporating the operational assumptions more commonly associated with institutional financial infrastructure: active liquidity management, controlled treasury operations, risk monitoring, and a strong emphasis on capital preservation alongside yield generation. The positioning allows the system to remain economically productive in today’s market environment while gradually aligning with the operational expectations of more traditional capital pools.

This extended into the surrounding operational layer required to support institutional participation responsibly. Identity verification, compliance coordination, and onboarding workflows were often treated as secondary during earlier cycles, but they become foundational as markets mature. Our collaboration with Keyring reinforced that layer, integrating compliance and identity infrastructure into the system architecture rather than treating them as external afterthoughts.

Over time, the distinction between crypto-native and institutional financial infrastructure will become less rigid. Hedge funds, asset managers, fintech platforms, payment companies, and eventually corporate treasuries are increasingly exploring how programmable settlement and digital dollar infrastructure can improve liquidity management and capital efficiency. When that convergence accelerates, the systems most likely to persist will not be the fastest-moving or the most ideological. They will be the systems that already speak the operational language institutional capital understands.

We did not set out to build a maximalist replacement for the existing financial system, and we did not assume institutions would migrate fully on-chain overnight. Financial systems rarely transform through abrupt replacement; they evolve through gradual integration, workflow adaptation, and the accumulation of trust. Elara was designed around a simpler observation: digitally native capital increasingly requires treasury infrastructure built with operational discipline from day one. That meant integrating compliance awareness into the architecture itself, treating reporting as a core layer rather than a downstream concern, and designing around sustainability rather than reflexive incentives. The market may still be early. The infrastructure increasingly cannot afford to behave that way.

How Viscous Becomes Fluid

Financial systems do not evolve uniformly. Their rate of change depends heavily on the surrounding environment.

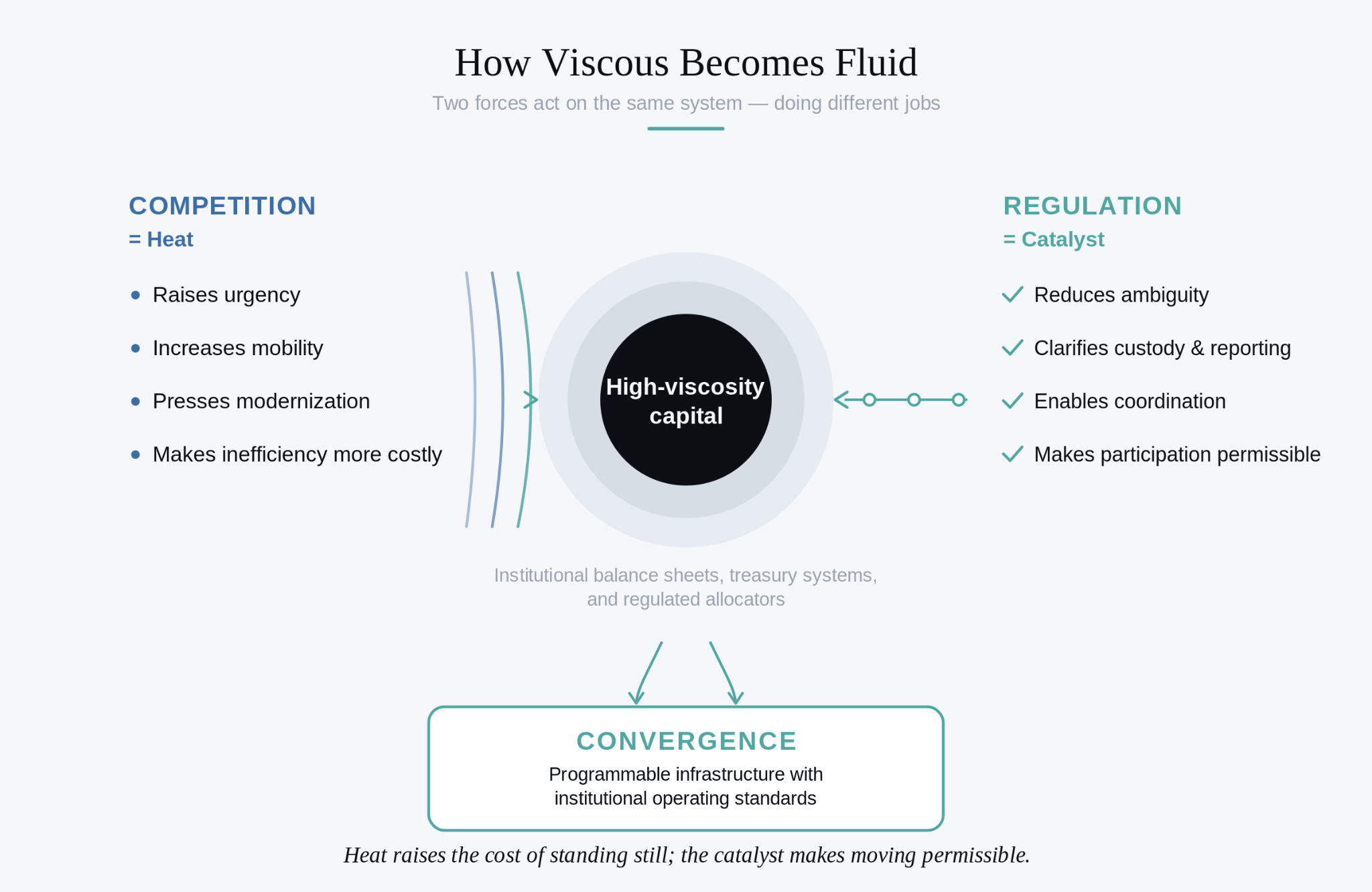

One of the more important developments over the past several years has been the gradual shift in regulatory posture toward digital asset infrastructure. Early regulatory conversation focused primarily on restriction and risk containment. More recent reforms have begun creating pathways for institutional participation rather than prohibiting it. It’s a critical shift. Financial systems rarely transform through technology alone. They change when legal, operational, and economic coordination begin aligning at the same time.

Regulation behaves less like a barrier and more like a catalyst. On its own, it cannot force adoption into existence. But once markets become sufficiently mature, regulatory clarity can accelerate institutional coordination considerably by reducing uncertainty around custody, reporting, settlement treatment, and fiduciary responsibility. This matters most in high-viscosity systems, where uncertainty itself functions as friction. Large financial institutions rarely avoid new infrastructure because they are unaware of it. More often, they avoid it because operational ambiguity creates unacceptable risk. Once that ambiguity narrows, adoption can shift surprisingly quickly.

Competition introduces a second force. In stable markets, institutional inertia can persist for years because the operational cost of change outweighs the immediate benefits of optimization. As competitive pressure intensifies, systems begin reorganizing. Competition acts as a form of heat, increasing the mobility of capital and pressing market participants to modernize treasury management, settlement infrastructure, and liquidity coordination.

This dynamic became foundational to how we thought about Elara. One of the central limitations of many earlier RWA models was the assumption that institutional capital would migrate on-chain because the infrastructure was theoretically more efficient. In practice, high-viscosity capital providers were being asked to move assets into environments that still appeared operationally fragile, governance-light, and reflexive under stress. The friction was too high relative to the perceived benefit.

Designing for the Convergence

We approached the problem differently. Rather than attempting to force institutional behavior into crypto-native systems prematurely, we built infrastructure capable of operating productively inside today’s digitally native markets while embedding the operational assumptions institutional allocators would eventually require.

This meant integrating compliance awareness into the architecture itself, and recognizing that trust, reporting, and risk management are not external constraints on financial infrastructure but part of the infrastructure. It also meant moving beyond reflexive incentive structures toward systems capable of sustaining economic utility through changing market conditions.

Durable financial systems rarely emerge through speed alone. They compound through reliability, repetition, and the gradual accumulation of operational trust. The objective was not simply to build for the market as it exists today, but for the conditions under which financial systems themselves begin to change. In that sense, Elara was designed less as a static product and more as infrastructure positioned for convergence. As digital asset markets mature and institutional participation expands, the systems most likely to persist will be those capable of translating between low-viscosity capital environments and the operational expectations of more traditional allocators.

We are not waiting for financial systems to become fluid. We are building infrastructure capable of managing both forms of flow. Elara is designed to operate within the high-velocity mobility of digitally native capital while remaining durable enough to support the slower, more deliberate movement of institutional balance sheets over time.