The Repricing

What the Co-Option Narrative Gets Wrong About Crypto's Evolution

Special Edition

This piece originally ran in The Bridge, my LinkedIn newsletter focused on institutional adoption and market structure.

Given recent conversations around token repricing, “co-option,” and what institutional adoption actually means for public networks, it felt worth sharing with the Interop audience as well.

The Narrative Taking Hold

A familiar story is circulating through crypto markets and financial media. Institutions have arrived, but not in the way many expected. Rather than buying tokens and validating the thesis that public blockchains would disintermediate traditional finance, they are building infrastructure themselves. Banks are tokenizing assets, sometimes on private ledgers. Asset managers are offering crypto exposure without requiring direct network participation. The institutions that were supposed to be disrupted are now laying the rails.

This moment is increasingly framed as a form of capture. Token prices, long treated as proxies for adoption and success, have fallen meaningfully from prior highs. Public blockchain ecosystems appear sidelined as incumbents adopt the technology on their own terms. The conclusion follows easily: crypto has been co-opted, and the open networks that once promised disruption are being rendered irrelevant.

This narrative is understandable, but naive. It reflects disappointment more than diagnosis. What we are witnessing is not co-option, but repricing, as markets develop a clearer understanding of what tokens do, and just as importantly, what they do not represent.

What It Actually Means to “Own” a Network

A persistent confusion in crypto markets concerns the relationship between token ownership and network ownership. When someone buys shares in a company, they acquire a fractional claim on that enterprise’s assets, earnings, and governance. Equity represents a legal right to residual cash flows and, in many cases, voting power over corporate decisions. The relationship between owning stock and owning a piece of the company is direct and well-defined.

Token ownership does not work this way. Holding ETH does not make someone a partial owner of Ethereum in any meaningful corporate sense. There is no entity called Ethereum, Inc. that issues dividends or reports quarterly earnings. The network is a protocol. It is a set of rules rendered across thousands of computers operated by independent parties. Owning tokens grants certain rights within that protocol, but ownership of the protocol itself is not something that can be purchased or transferred.

This distinction matters because much of the disappointment around token prices stems from a category error. If you believed that owning tokens meant owning the network, then institutional adoption of blockchain technology should have made you rich. After all, when a technology becomes widely adopted, the owners of that technology benefit. On the contrary, token holders are not owners of the technology. They are participants in the network who hold certain usage rights and, in some cases, claims on protocol-defined rewards.

The confusion is not entirely the fault of individual investors. Early marketing around crypto assets often implied or stated outright that token ownership was analogous to equity ownership in a new kind of internet infrastructure. The language of “investing in Ethereum” or “owning a piece of the future” encouraged this misunderstanding. Markets are now correcting for it.

Tokens as Rights to Future Blockspace

If tokens do not confer ownership, what do they actually represent? For Layer 1 blockchains, the most accurate framing is that tokens are rights to future blockspace. Every blockchain has a finite amount of computation and storage that can be processed in each block. Tokens function as the currency required to access that capacity. To execute a transaction, deploy a contract, or store data on the network, you need tokens to pay for the blockspace your activity consumes.

This framing clarifies both the value and the limitations of token ownership. Tokens are useful insofar as you need to use the network. If you are building an application, moving assets, or interacting with protocols, you need blockspace, and blockspace requires tokens. The value of holding tokens, then, is tied to anticipated demand for blockspace on that particular network.

For proof-of-stake networks, tokens also provide access to staking yield, or rewards distributed to validators who lock up tokens to secure the network. This yield is real and represents an additional source of value beyond blockspace access. But staking rewards are not dividends. They are compensation for providing security services to the network, denominated in the network’s native token. The value of those rewards depends on both the token price and the sustainable economics of network security.

Understanding tokens as blockspace rights rather than ownership claims helps explain why increased usage does not automatically translate into proportional token price appreciation. A busy network with high demand for blockspace may indeed see elevated token prices, but the relationship is mediated by supply dynamics, fee structures, layer-2 scaling solutions, and competition from alternative networks. More activity is not the same as more value accruing to token holders.

Why Usage and Value Accrual Are Not the Same Thing

The expectation that network usage would drive token prices rested on a simple model: more users means more demand for tokens, which means higher prices. This model has proven incomplete. Usage can increase substantially while token prices stagnate or decline, and understanding why requires examining the actual mechanics of value capture.

First, many blockchain networks have actively worked to reduce transaction costs. Lower fees are good for users and application developers but reduce the per-transaction demand for tokens. Second, scaling solutions (whether layer-2 networks, rollups, or alternative execution environments) can absorb usage that would otherwise occur on the base layer, potentially reducing fee pressure on the main chain. Third, competition among blockchains means that usage growth may be distributed across multiple networks rather than concentrated in one.

There is also a timing mismatch between usage growth and value accrual. In traditional equity markets, a company’s stock price theoretically reflects the present value of all future cash flows. For tokens, there is no equivalent cash flow to discount. Token prices instead reflect a complex mix of speculative interest, utility demand, and monetary premium. Increased usage may eventually manifest in higher prices, but the transmission mechanism is neither direct nor guaranteed.

This does not mean tokens are worthless or that usage growth is irrelevant. It means that the naive model (buy tokens, wait for adoption, collect returns) was always too simple. Value accrual in blockchain networks follows different paths than value accrual in traditional corporate structures, and markets are learning to price that difference appropriately.

The Fear and Reality of Incumbent-Owned Chains

One version of the co-option narrative focuses specifically on private or permissioned blockchains operated by traditional financial institutions. The fear is that banks will build their own closed networks, capture the efficiency benefits of blockchain technology, and leave public networks irrelevant. In this view, JPMorgan’s Onyx or Goldman’s digital asset initiatives represent existential threats to Ethereum and its peers.

The reality is more nuanced. Private chains serve specific purposes and have real limitations. They work well for known counterparties operating within established legal frameworks who need shared infrastructure for settlement or record-keeping. They are less suited for open innovation, permissionless participation, or applications that require credible neutrality.

More importantly, the relationship between private and public infrastructure is not zero-sum. Institutions building private systems often rely on public networks for certain functions, be that interoperability, access to liquidity, or settlement finality. A tokenized bond might be issued on a permissioned chain but settled using a public network. A private payment system might use a public blockchain as a backstop or bridge to other systems.

The question is then not whether institutions will use blockchain technology (they clearly will) but what role public networks will play in that adoption. The answer appears to be: a meaningful but not exclusive role. Public blockchains provide properties that private chains cannot replicate, including censorship resistance, open access, and the network effects that come from permissionless participation. These properties are valuable for some use cases and irrelevant for others.

Public Blockchains as Innovation Substrates

The most important function of public blockchains may not be settlement or payments but something harder to quantify. They serve as open environments for financial innovation. Public networks allow anyone to deploy applications, experiment with new mechanisms, and compose existing components into novel structures. This permissionless experimentation has produced everything from automated market makers to flash loans to complex derivatives. These innovations emerged without anyone’s permission or prior approval.

This function is valuable precisely because it is difficult to replicate in traditional financial infrastructure. Regulated institutions cannot easily experiment with novel financial instruments. Compliance requirements, approval processes, and liability concerns create friction that slows innovation. Public blockchains serve as a kind of regulatory sandbox, not in the formal sense of a government-approved testing ground, but in the practical sense of a space where new ideas can be tried without gatekeepers.

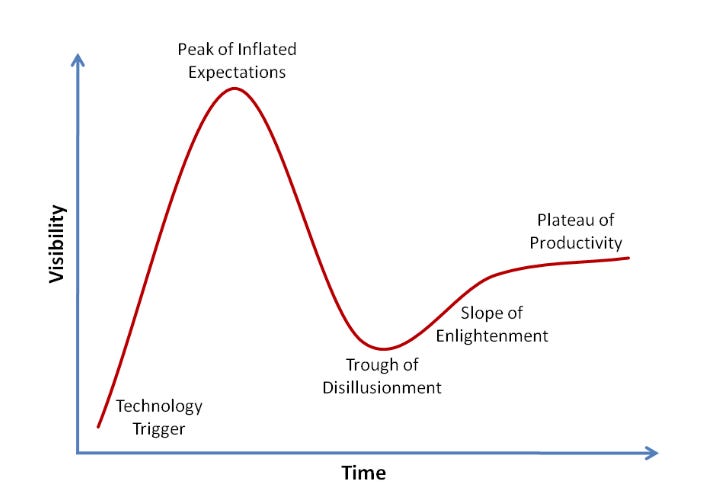

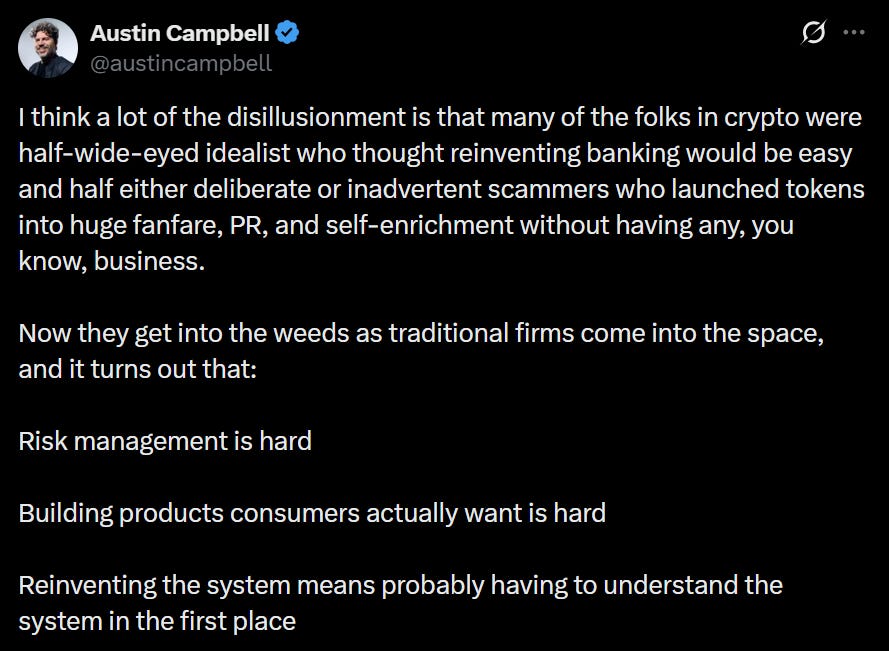

Many innovations that begin on public networks eventually migrate to more controlled environments. Ideas proven in permissionless settings get adopted, refined, and implemented within regulated frameworks. This is not co-option but diffusion and places us somewhere in Gartner’s Trough of Disillusionment above. It is the normal process by which successful innovations spread from experimental contexts to broader use. The value of the experimental substrate lies not in capturing all the value of innovations that emerge from it, but in enabling those innovations to emerge at all.

Public blockchains, understood this way, function less like companies to be invested in and more like public goods to be used. They provide infrastructure that enables activity, and the value of that infrastructure is not fully captured by any single participant, including token holders. This framing is less exciting than the promise of owning a piece of the future financial system, but it is more accurate.

The Structural Difference Between Tokens and Equity

Token holders often compare their position to that of early equity investors in transformative technology companies. The analogy is appealing: Amazon shareholders who held through volatility were rewarded handsomely. Why shouldn’t the same be true for early participants in blockchain networks?

The structural differences are significant. Equity represents a legal claim on corporate profits. When Amazon succeeds, shareholders benefit because the company’s earnings accrue to them. Tokens generally carry no equivalent claim. When a blockchain network “succeeds,” there is no automatic mechanism that transfers that success to token holders. Usage fees may flow to validators or be partially burned, depending on the network’s design, but this is fundamentally different from dividends or buybacks funded by corporate profits.

Governance follows a similarly different logic. In corporate structures, decision rights are clearly defined, even if power is concentrated in practice. Shareholders understand what they can vote on, which decisions sit with management or the board, and where legal accountability ultimately resides. In blockchain networks, governance is far less uniform. Decision-making may be split across DAOs, foundations, core development teams, validators, and informal social consensus. What token holders can influence, and how that influence is exercised, varies widely by network and over time.

This ambiguity is not a flaw so much as a design choice, but it has consequences for valuation. An asset with uncertain and fragmented decision rights, and no clear claim on cash flows, should not be valued as though it confers ownership of a coherent enterprise. Assets with fewer rights and weaker claims on value creation should, all else equal, be worth less than assets with stronger rights and clearer claims.

Markets are adjusting to that reality. Tokens are being repriced not because the underlying technology has failed, but because expectations about what token ownership actually entails are becoming more precise.

What This Moment Actually Represents

The current period in crypto markets is often described in terms of failure or capture. Prices have fallen from highs. Institutions have not embraced public tokens as expected. The revolutionary promise seems diminished. This framing misses what is actually occurring.

Markets are not rejecting blockchain technology. They are developing a more accurate understanding of the relationship between technology adoption and token value. These are different things, and conflating them led to mispricing in both directions. We have experienced excessive optimism when adoption narratives were ascendant, and excessive pessimism when the limitations of token value capture became apparent.

The technology continues to develop. Applications continue to be built. Institutional adoption of blockchain infrastructure continues, even if it doesn’t always involve public tokens. What is changing is the market’s model for pricing participation in these networks. That model is becoming more realistic about what tokens represent, what rights they confer, and how value flows through decentralized systems.

This is not a failure in execution but a maturation narrative. Early markets for any new asset class tend toward mispricing as participants work out what the assets actually are and how they should be valued. The dot-com era saw similar dynamics. Technology companies were real and valuable, but initial value models were often wrong. The correction was painful but necessary for building sustainable markets.

Crypto is undergoing its own version of this correction. Tokens are being repriced to reflect their actual economic role: rights to blockspace, claims on staking yield, and participation in networks that may or may not capture value in proportion to their usage. This repricing does not mean crypto has failed or been co-opted. It means markets are learning. That process is uncomfortable for those who bought at higher prices, but it is also necessary for the asset class to develop sustainable foundations.

The path forward requires clarity about what public blockchains are for and what token ownership actually provides. Public networks serve as open infrastructure for innovation and as settlement layers for activities that benefit from decentralization. Tokens provide access to that infrastructure and, in some cases, yield from securing it. These are real and valuable functions, but they are different from owning equity in a technology platform. Market participants that understand this distinction will price tokens appropriately. Those who don’t will continue to suffer from the heavy price action that comes from mismatched expectations.